The Bank of England and Chancellor Jeremy Hunt has failed to reduce interest rates and the tax burden quick enough, a former Bank of England adviser has claimed.

Dr Roger Gewolb said Britons’ finances are “being crushed unnecessarily” as the base rate looks likely to remain at a 16-year-high and the tax burden stands at its highest rate since World War II.

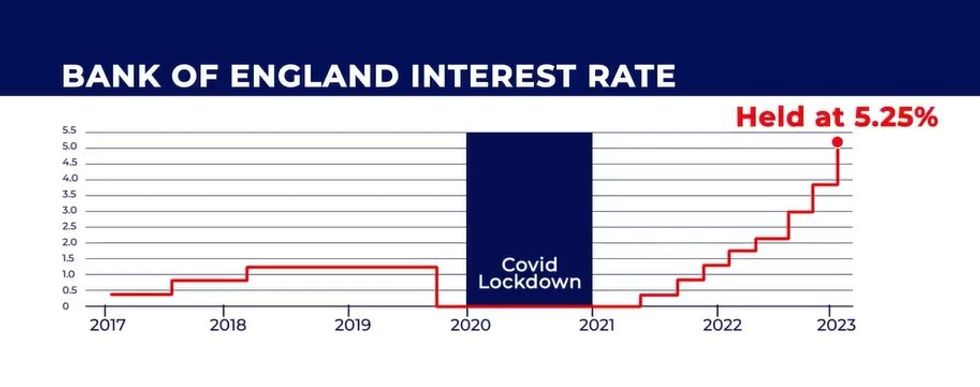

As it stands, the central bank’s base rate is held at 5.25 per cent, following 14 consecutive rises between December 2021 and August 2023 to try to ease inflation.

Despite the Consumer Price Index (CPI) rate easing to four per cent, the Bank is expected to keep interest rates at their current level this week which comes as a blow to homeowners and borrowers.

In recent months, Mr Hunt has unveiled cuts to capital gains tax on property and the National Insurance rate, but experts have warned fiscal drag is diminishing savings made by these rate reductions.

Fiscal drag is the term used to describe when wages rise while tax allowances stay the same. As a result, taxpayers are dragged into higher brackets which causes them to pay more to HMRC.

Do you have a money story you’d like to share? Get in touch by emailing money@gbnews.uk.

Experts are taking aim at the Chancellor and central bank for their handling of the economy

GETTY/GB NEWS

According to Dr Gewolb, the Government and Bank of England are failing to prevent families from being “crushed” by the growing tax burden and interest-hiked repayments.

The former Bank of England adviser explained: "We are being crushed. Unnecessarily. Andrew Bailey, Governor of the Bank of England, refuses to lower interest rates.

“Chancellor Jeremy Hunt refuses to lower taxes. All Britons are suffering because of inept leadership, and Labour is not offering any viable or even clear alternatives.

“Bailey never should have raised the base rate 14 times in the first place. We don’t have consumer-driven inflation and food and energy prices have now fallen by themselves, as they always do.

“Nothing to do with consumer spending. Unbelievable to crush British households and businesses so viciously and for so long with these hikes with no effect, even though Bailey, Hunt, and Sunak are now claiming the credit for inflation falling of course.”

He cited that 500,000 businesses are reportedly close to failing and mortgage arrears are up 50 per cent due to the increase to interest rates.

During the Spring Budget, the Chancellor noted that a worker on the average salary would save a combined £900 from the last two cuts to the National Insurance.

However, Mr Hunt also confirmed tax thresholds would be frozen until at least 2028 during his Autumn Budget last year.

Dr Gewolb believes the Chancellor “has not fooled anyone” when it comes to the policies he has implemented during his time at the Treasury.

The financial entrepreneur added: “His myth that we cannot afford this disappears when we stop paying £40billion per year to ourselves, from one pocket to another, for interest on the gazillions of money that the Bank of England printed.

LATEST DEVELOPMENTS:

The Bank of England base rate is at a 15-year high of 5.25 per cent GB NEWS

The Bank of England base rate is at a 15-year high of 5.25 per cent GB NEWS“This incredible self-inflicted harm to our economy has been strongly criticised by the Reform party and many think tanks and eminent economists. Switzerland doesn’t do this, nor do the European Central Bank and many others.

“And that £40billion is exactly enough to raise the lower income tax threshold from £12,570 to £20,000 per year, alleviating the fiscal drag that is hurting millions and millions of people unnecessarily, whilst building up a Tory war chest.”

The Bank of England’s Monetary Policy Committee (MPC) will announce any changes to interest rates on Thursday, March 21.

National Insurance will be slashed to eight per cent for workers and six per cent for the self-employed from April.