A shocking graph reveals millions of low-earning retirees could pay tax on their state pension as soon as next year as frozen thresholds push basic payments over the tax-free allowance.

Each April, the state pension rises in line with the ‘triple lock’ policy, which guarantees an increase based on the highest of three measures: 2.5 per cent, inflation, or average earnings growth.

Currently, no income tax applies to state pension payments, which are due to climb to £11,973 annually for those receiving the full new state pension this April, since this amount remains under the £12,570 tax-free personal allowance.

Earlier projections from the Office for Budget Responsibility (OBR), published with the Budget, had suggested that state pension payments wouldn’t surpass the personal allowance until April 2027.

However, Deutsche Bank forecasts that the full state pension could rise to £12,631 next year, surpassing the personal allowance threshold.

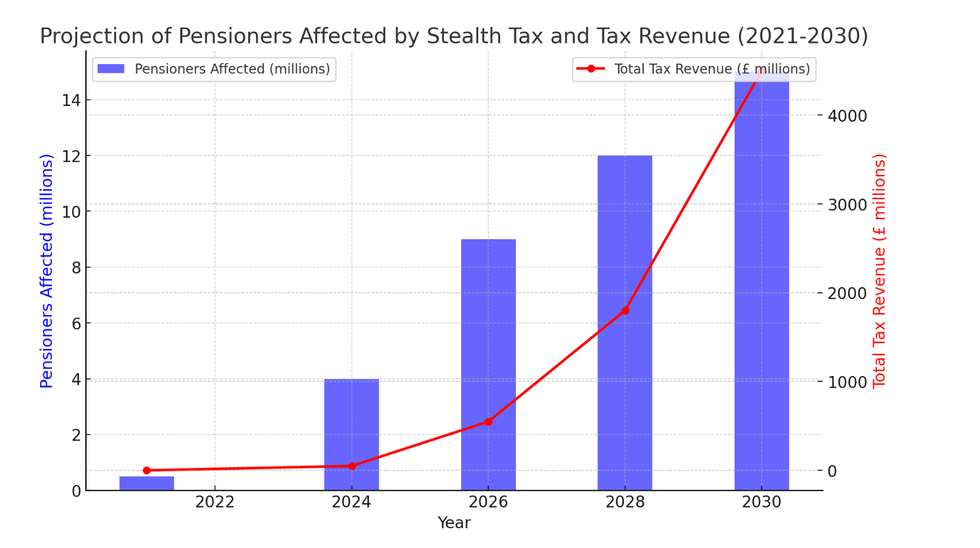

According to the bank's analysis by Deutsche Bank, approximately nine million pensioners will be paying tax on their income from April 2026 due to this change (see graph below)

Graph projects the number of retirees facing a stealth tax on their state pensions will rise in the coming years

Chat GPT

How much will you owe?

The impact of the stealth tax changes will depend on your total taxable income.

If you receive close to but below the full state pension, your total income will likely remain under the £12,570 personal allowance, so you won’t pay income tax.

However, under the changes, low-earning retirees receiving the full state pension would have £61 of their income subject to taxation.

At the basic income tax rate of 20 per cent, this results in an annual tax liability of £12.20.

The more private pension income you have, the more tax you’ll owe. For example, if you receive £9,000 from the state pension plus £4,000 from a workplace/private pension, your total income would be £13,000.

Since the personal allowance is frozen at £12,570, £430 would be taxable, and at the 20 per cent tax rate, you’d pay £86 in tax.

Based on current trends, the number of pensioners facing the stealth tax will rise in the coming years as the state pension increases while the personal allowance remains frozen (see above chart).

In 2021-22, approximately four per cent of pensioners had incomes exceeding the threshold. This figure rose to around 11 per cent in 2024-25 and is projected to reach over 43 per cent by 2029-30, according to research from Age UK.

The Institute for Fiscal Studies (IFS) has also highlighted how the share of those aged 65 and over who pay income tax has risen dramatically over a wider period, from 36 per cent in 1990–91 to 62 per cent in 2022–23.

LATEST MEMBERSHIP DEVELOPMENTS

Chancellor Rachel Reeves is facing growing calls to take immediate action to protect pensioners

GB NewsAhead of her Spring statement, Chancellor Rachel Reeves is facing growing calls to take immediate action to protect pensioners.

Silver Voices, a leading pensioner advocacy group, wants the personal allowance to be increased by £1,000 from April for pensioners, with future uprating linked to the triple lock.

Dennis Reed, the director of Silver Voices, said: "The Chancellor must take urgent action to prevent the basic state pension from being taxed from April 2026."

He warned the situation would be "ludicrous" as the state pension safety net has already been paid for through national insurance contributions and taxes.