Britons are being warned that money kept in millions of bank accounts “losing value every day”, according to experts.

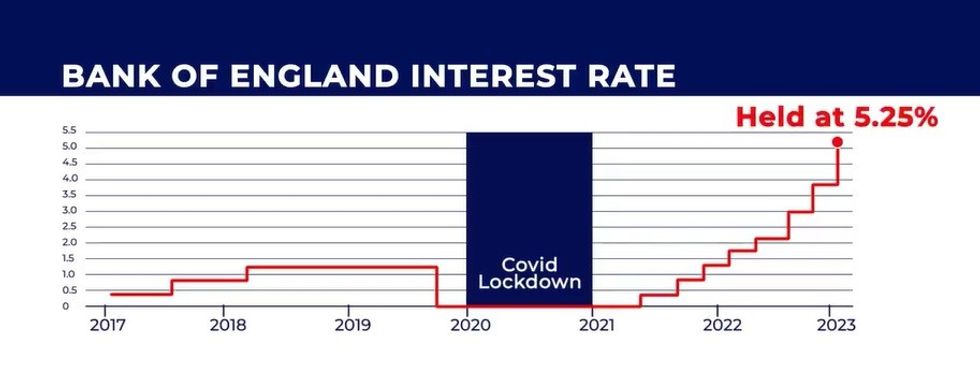

Savers have benefited from the Bank of England’s decision to raise the base rate to 5.25 per cent as it attempts to ease inflation.

Despite 14 consecutive rate hikes from the central bank, experts from TotallyMoney are sharing why not everyone has been able to benefit from better returns on their accounts.

The financial institution is highlighting how high street banks and building societies have been slow to pass on this interest rate rise to their customers.

Last summer, the Financial Conduct Authority (FCA) outlined a 14-point action plan for banks to follow on cash savings.

As well as this, the regulator launched a £600,000 campaign to encourage savers to switch accounts in February.

Do you have a money story you’d like to share? Get in touch by emailing money@gbnews.uk.

Experts are warning money in bank accounts is "losing value"

GETTY

In a survey conduct by TotallyMoney, 56 per cent of British adults shared they have either stopped saving, lowered their amounts or used deposits to cover expenses in response to the cost of living crisis.

While 70 per cent of respondents, the equivalent of 37.1 million of the population, still have a savings account with a bank in some capacity, the type of account varies per person.

Some 54 per cent of these are held with savings accounts, building societies or NS&Is, while 28 per cent keep their money in cash ISAs, and 26 per cent invest in Premium Bonds.

Notably, 37 per cent of savers have not switched for five years with a staggering 27 per cent having never switched.

Out of those polled, around 52 per cent of savers have switched in the past or plan to switch accounts in the future.

Alastair Douglas, the CEO of TotallyMoney, warned bank customers to be alert their hard-earned cash could be “losing value”.

He explained: “In recent months, the UK’s biggest banks have banked billions of pounds and recorded record profits from charging high rates on debt while paying low interest on savings.

“And with inflation at four per cent — still double the target rate — some are paying as low as 1.16%, meaning some deposits are losing value every single day.

“But millions of customers unwittingly think their banks are doing right by them, and a quarter haven’t switched accounts because they trust their bank.”

According to the Douglas, customers remaining loyal to their banks “doesn’t pay” and Britons should shop around for the best deal that will bolster their finances.

LATEST DEVELOPMENTS:

The Bank of England has held the base rate at 5.25 per cent in recent months GB NEWS

The Bank of England has held the base rate at 5.25 per cent in recent months GB NEWSThe money saving expert added: “So work out which savings option works best for you, and switch accounts to a provider who’ll help your money grow.

“While the regulator is right to campaign for people’s money to work harder, they should be pushing banks, not people to change.

“The role of the Consumer Duty is to set higher and clearer standards of consumer protection across financial services, requiring firms to put their customers' needs first. Not vice versa.”

The Bank of England's Monetary Policy Committee (MPC) will next make a decision regarding interest rates on May 9, 2024.