HMRC is set to rake in billions of pounds as an ongoing stealth tax and higher interest rates leave millions of savings accounts at risk of triggering a tax bill.

In April, more than six million savings accounts were set to activate a tax bill this year, according to analysis by Shawbrook.

It’s more than twice the three million accounts at risk of being taxed in April 2023.

Basic rate taxpayers can earn £1,000 of interest tax-free each year, while higher rate taxpayers are limited to earning £500 of annual interest. Higher-rate taxpayers have no tax-exempt savings allowance.

Frozen tax thresholds, which are dragging more people into the basic and higher rate tax brackets as income rises, and higher interest rates have led to a dramatic increase in savers exceeding their personal savings allowances.

It means a basic rate taxpayer earning £2,000 in interest could be slapped with a £200 tax bill, rising to £600 for higher rate taxpayers and £900 for additional rate taxpayers.

AJ Bell’s personal finance director Laura Suter warned the amount Britons are paying in tax on savings interest has “spiralled” in recent years.

The latest forecast indicates £10.4billion will be paid in tax on savings interest this tax year, up from £1.4billion collected in 2021/22.

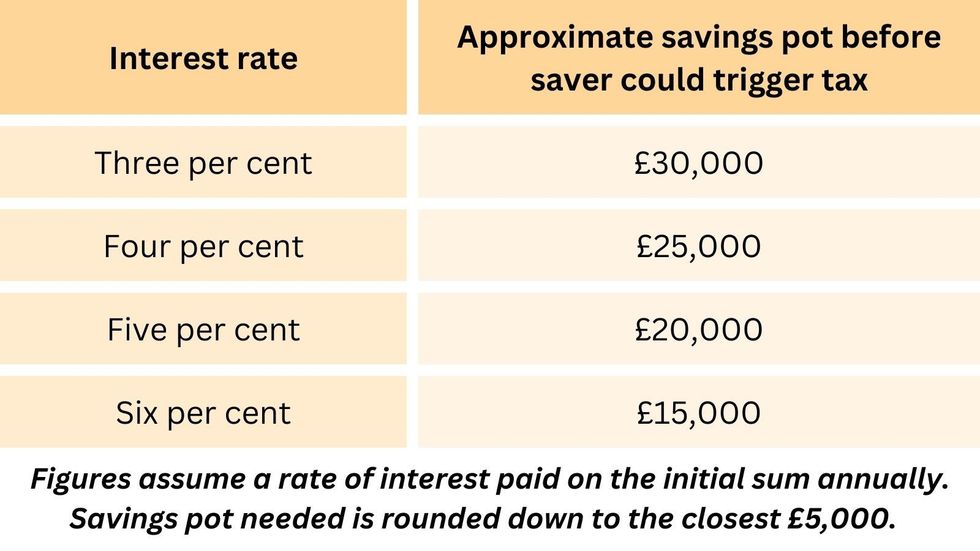

AJ Bell has shared a rough guide on the size of savings a basic rate taxpayer with a £1,000 personal savings allowance could have before they have to pay tax, according to different interest rates.

AJ Bell worked out the approximate savings pot a person could have before triggering tax for different interest rates. Those on the lowest income may have a £5,000 starting rate allowance.

AJ BELL | GB NEWS

Suter said part of the issue is "people not using ISAs to protect their cash savings".

She explained: "Rates can be fractionally higher outside an ISA, but for those people who find they breach the personal savings allowance, it could be a false economy if the extra interest is overshadowed by the tax bill.

“Another factor is frozen tax bands, which means more people are being pushed into higher tax bands and see their personal savings allowance cut in half as a result. Some lose it altogether if they find themselves paying additional rate tax.

“If you find yourself losing your tax-free allowance on cash interest because your salary goes up, you could find you’re both paying tax on savings and doing so at a higher rate of taxation."

Rachel Springall, finance expert at money comparison website moneyfactscompare.co.uk, told GB News it is “imperative” savers take some time to check the interest they earn on their savings pots, to ensure it doesn’t breach their own allowance.

She added: “It may be more likely the interest triggers a tax bill now compared to previous years due to higher interest rates.”

Do savers need to contact HMRC?

Those who think they have already breached or will breach the personal savings allowance may wonder whether HMRC will chase them for a tax bill.

Finance expert Rachel Springall told GB News: “Savers who think they are on course to breach their personal savings allowance during a tax year can inform HMRC before the savings provider calculates the interest earned, which is confirmed to HMRC.

“To avoid paying tax back as a single lump sum, HMRC would normally change someone’s tax code for the following year, so the extra tax is taken from any income over the course of that year.

“If savers feel they have paid too much tax, they can claim a refund using form R40, which consumers can do for the current or previous tax years.

“Those who self-assess can report any savings or investment income as part of the usual tax return.”

The tax that savers would need to pay on fixed bonds can vary depending on the terms, Springall explained.

However, HMRC states that tax is payable “when it is received or made available to the recipient".

Springall explained: “As an example, if a saver has their interest paid out as income, then the savings paid will be liable for tax at that point.

“It’s worth checking the total interest projected to be earned when a bond matures as it could exceed the PSA for that year.”

Tax allowances on savings interest

Most people can accrue some interest from their savings without being taxed on it.

The annual tax-free savings allowances, which reset each tax year, include:

- The personal allowance

- Starting rate for savings

- Personal savings allowance

If the personal allowance isn’t used up on income, such as wages or pension, then a saver can earn interest tax-free up to their personal allowance. The standard personal allowance is currently £12,570.

A person may also qualify for the starting rate for savings – which allows for a maximum £5,000 of interest tax-free – but this allowance reduces as earnings from other income rises.

People with other income of £17,570 or more are not eligible for the starting rate for savings.

Springall explained: “Low income earners can also benefit from a zero per cent ‘starting rate’ of income tax for up to £5,000 of savings interest.

“This reduces for every £1 earned over the personal income tax allowance of £12,570 (2024/25 tax year).”

The personal savings allowance lets basic rate taxpayers – which refers to people earning between £12,571 and £50,270 (the tax bands are different in Scotland) - to earn up to £1,000 tax-free.

Springall explained: “It means savers will only have to pay tax on savings interest above this amount.”

Higher rate taxpayers - who pay 40 per cent tax on annual income between £50,271 and £125,140 – get a reduced limit of £500.

Additional rate taxpayers, who are taxed at 45 per cent on income over £125,140, have no tax-exempt savings allowance.

MORE FROM GBN MEMBERSHIP:

An ISA is a tax-free savings wrapper

GETTY

What is an ISA?

An ISA, which stands for Individual Savings Account, is a tax-free savings wrapper.

The maximum amount a person can deposit into ISAs each tax year is £20,000. The money can be put into one account or the allowance can be split across multiple accounts.

There are four types of ISA – cash ISA, stocks and shares ISA, innovative finance ISA and Lifetime ISA.

The latter, Lifetime ISA, has its own specific rules and an annual limit of £4,000, and this is included within the ISA annual allowance of £20,000.

Springall said: “Those looking to avoid paying tax on their savings would be wise to utilise their ISA allowance each year. Investing in cash ISAs protects money from tax and it does not impact the PSA.

"These can be very useful for savers both over the short and long-term, however, using a stocks & shares ISA could reap more returns over the longer-term, but these also come with risks.”

Adam Thrower, head of savings at Shawbrook, also highlighted the tax-free benefits of ISAs.

He said: “Savers might want to consider fixed-term ISAs, locking in high rates for a year longer.

“With the Bank of England’s interest rates likely to have peaked, there is growing anticipation of the first cut for some time, and when it does arrive this could reduce interest rates offered on savings.

“Locking in now could secure higher interest rates for the longer team, and using ISAs to do that can keep your money free from any surprise tax bills.”