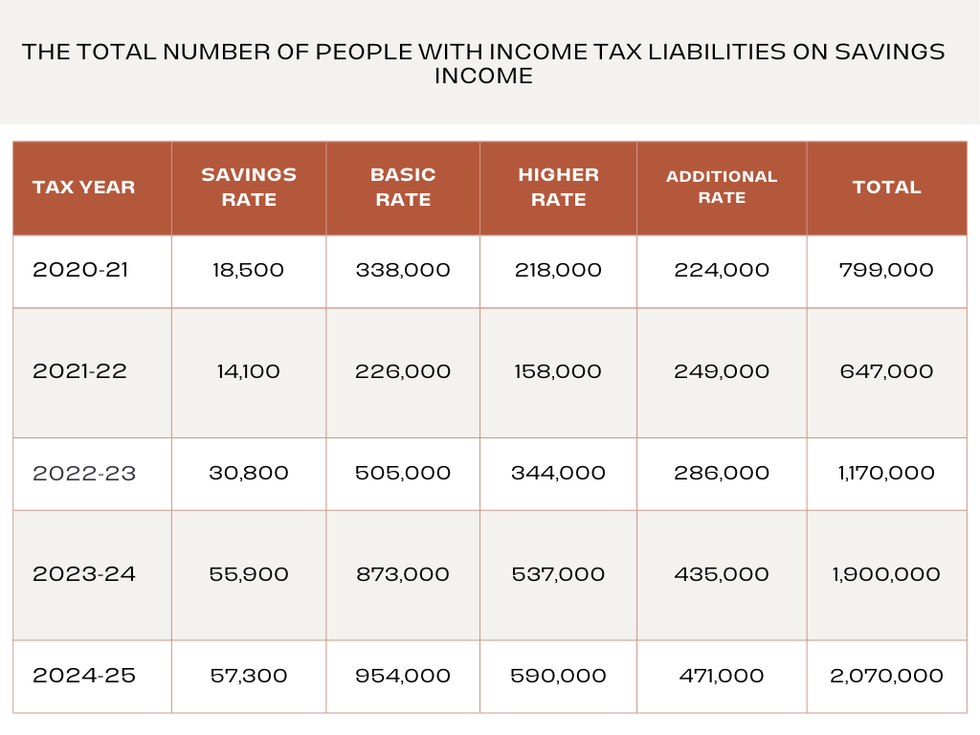

More than two million people will face tax bills on their savings interest this tax year, as rising interest rates and frozen tax thresholds push more savers into paying tax.

The figure represents a dramatic increase from just 650,000 people three years ago, according to research by AJ Bell, with analysts blaming this phenomenon on the impact of fiscal drag.

This is the term used to describe when tax allowances are frozen over a period of time when either inflation or wages are rising, resulting in workers being pulled into higher brackets.

"While it might be too late to solve the problem for the current tax year, you can organise your savings and dodge some sneaky tax traps to avoid being landed with an unexpected tax bill next year," says Laura Suter, director of personal finance at AJ Bell.

The impact is particularly stark for basic-rate taxpayers, with nearly one million expected to pay tax on their savings this tax year. This marks a significant jump from just half a million basic-rate taxpayers affected in 2022/23.

Do you have a money story you’d like to share? Get in touch by emailing money@gbnews.uk.

Britons could be hit by a tax on savings interest

GETTY"The thorny issue is that lots of people won't realise they owe tax until a brown letter lands on their doormat," warns Suter. For those on PAYE, HMRC calculates any tax liability based on information provided by banks and building societies.

This often results in tax code adjustments, with the tax being repaid through monthly payslips, reducing take-home pay, according to AJ Bell.

"Lots of people may have racked up a hefty tax bill already this year, because they didn't realise they'd breached their Personal Savings Allowance," explains Suter.

Those completing self-assessment tax returns must declare any savings interest and subsequent tax due themselves.

Some 2.07 million people expected to pay tax on their savings this yearHMRC

Some 2.07 million people expected to pay tax on their savings this yearHMRCThe Personal Savings Allowance introduction led many savers to avoid ISAs, a decision that is now affecting their finances.

The £20,000 annual ISA limit, while generous, may prove insufficient for those who have accumulated significant savings outside these tax-efficient accounts.

"Since the introduction of the Personal Savings Allowance lots of savers shunned ISAs. But that decision is hitting savers pockets now, as many find they have too much money to move it into an ISA in one year," says Suter.

Experts advise savers to consider moving cash into ISAs if they have remaining allowance this tax year.

Those with partners could split cash savings between them to utilise both ISA allowances.

"If your partner pays income tax at a lower rate, it might make sense to move any savings that will attract tax into their name," suggests Suter.

LATEST DEVELOPMENTS:

Savers can save tax-free with Individual Savings Accounts (Isas)PEXELS

Savers can save tax-free with Individual Savings Accounts (Isas)PEXELSShe cautions: "Just make sure the savings interest doesn't tip them into the next tax bracket and undo all your good organising work."

Notably, Suter cited how fixed-rate savings accounts could be considered a tax trap, stating: "Many savers are locking into fixed-rate accounts for guaranteed returns, but few realise the tax risk.

"Interest is taxed when it becomes accessible, so if your account pays at maturity, years’ worth of interest lands in one tax year, potentially pushing you over your Personal Savings Allowance.

"Longer-term accounts are most at risk. For example, £7,000 in a top three-year fix at 4.63 PER CENT would generate £1,018 interest at maturity, exceeding a basic-rate taxpayer’s £1,000 Personal Savings Allowance. To avoid this, choose an account that pays interest monthly or annually, or opt for a fixed-term ISA to keep your interest tax-free."