Interest rates are at their highest level since 2008, and while inflation has been easing in recent months, Ofgem’s chief executive has warned many will face energy bills similar to last year, and for some, it'll be even worse this year than last.

Making money work harder is more important than ever, be it accessing the best interest rate on savings accounts or making spending stretch further.

As more and more people brace for more tough money decisions this winter, TV presenter and financial adviser Emmanuel Asuquo sat down with GB News to share some of his top money tips.

First of all, he warned those who have savings, or some money left over each month to save, may find seeking the top interest rates can pay off.

Emmanuel Asuquo said savers might be able to get into a savings habit via schemes such as Help to Save

|EMMANUEL ASUQUO

“There are different types of accounts – and the rates have gone up recently,” he said.

“There are loads of instant access savings accounts that are paying around five per cent or more. So that’s really good.

“There are also regular savers so if you are someone who maybe doesn’t have a lump sum but you know you have money leftover each month, there are some accounts paying seven or eight per cent.

“They limit how much you can put in there – some are £200 or £300 a month. But even if it’s £50, for me, it’s all about getting into the habit of saving.

“Once you get into the habit of saving, you can increase how much you save over time.

“Right now, interest rates are high. We talk about it when it comes to mortgages and complain our mortgages are going up, but it’s a great time for savings. So if you are someone who has money left over each month or has savings, now is the time.”

Mr Asuquo also highlighted a savings option which provides a 25 per cent boost to savings, known as Help to Save. HMRC says more than 359,200 people have opened an account since the scheme launched in September 2018 and a further three million savers could still benefit.

The government-backed savings scheme is intended for people who are on a low income and provides a 50 pence bonus for every £1 saved in the account over four years.

Savers can put between £1 and £50 into the account each calendar month, and deposits don’t need to be made each month. This means the maximum amount which can be saved is £2,400 over four years, meaning a potential bonus of £1,200.

Mr Asuquo said: “Help to Save is a really good scheme for people on low incomes, people who struggle to save, who don't have that much money left over.

“If you can save and you can put that money away and not touch it for a longer time, the amount you get back from the government on top, I think it's a great scheme and people should really look into it.”

He explained while it’s not a “huge amount” which can be deposited each month, it can help to build a pot of savings.

The money expert continued: “Saving for me is about a habit. This gets you into the habit and, especially for people who may be struggling now with the cost of living crisis, saving seems like such a far-away thing to be able to do. I think Help to Save really allows you to get in there, get saving, get into the habit, get a good amount of money back from your savings and based on how much you put in, much better than what you get on the typical savings account.”

While many people who are struggling will already be sticking to a tight budget, some people who are feeling the rising cost of living may benefit from planning ahead - and the financial adviser shared some tips on this.

Mr Asuquo said: “The biggest tip I always tell people is to make a plan. One of the things we tend to do is we don’t actually take the time to plan our spending.

“We tend to go to the same shops and buy the same things and feel like we don’t need a shopping list, we don’t need to make a plan. We go, we see the yellow stickers, we smell an amazing bakery, and all of a sudden our money is gone and the budget is blown. It’s really important to have a budget.”

Mr Asuquo also stressed the importance of shopping around.

“Sometimes we are so loyal to certain companies or certain brands but actually it’s not in our interests. It’s really important to shop around and check. There are comparison websites online where you can compare stuff, so take the time.”

Renting or borrowing items rather than buying them could also help people reduce their outgoings and save more money each month, with new research from car leasing experts ZenAuto showing 93 per cent of Britons have borrowed rather than bought everyday items.

What’s more, nearly half of those asked (42 per cent) said they’re more likely to impress their friends with money they’ve saved, rather than what they’ve spent on something.

The research found those who have embraced the leasing lifestyle claim to be saving an average of £449 on tech appliances, £425 on furniture and £472 on DIY equipment each year.

Mr Asuquo, who has teamed up with ZenAuto to offer tips and advice on how to pay less and do more, said: “The access economy comes as a welcome alternative to avoiding high one-off costs and owning outdated technology.

“You can experience the latest products without exceeding your budget to acquire them and you also tend to pay a fair price, based on your actual usage of them.

“Not only this, but a new car, for example, loses value as soon as you drive it off the forecourt, losing up to 40 per cent by the end of the first year. Similarly, phones depreciate to a fraction of their original value in two years.

“When your products are no longer useful to you or are outdated for your needs or lifestyle, you can return them at the end of your contract. This can be a positive for the environment too, as it means it will likely be re-purposed in one way or another once you’re done with it, rather than collecting dust somewhere in your home.”

Mr Asuquo said a lot of people have found they have saved money by borrowing clothes, for example.

He said: “Rather than buy a new outfit, you can rent a new outfit, and the same thing when it comes to certain furniture in the house.

“We are a generation who likes to be on trend, we don’t want to own things that have fallen out of date.

LATEST DEVELOPMENTS:

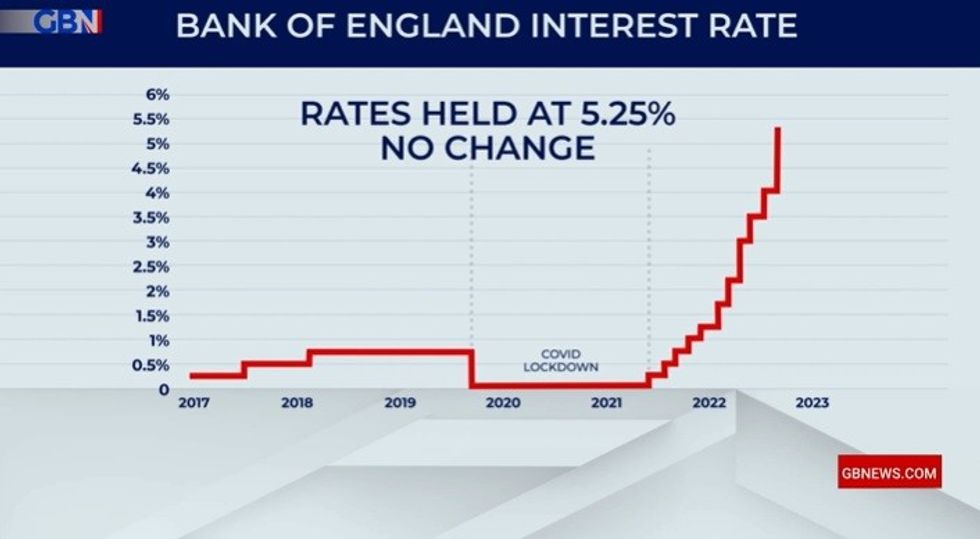

Interest rates on savings accounts have been rising as the Bank of England has hiked the base rate 14 consecutive times in the past two years

|GB NEWS

“But if the trends change quickly and if you’re always having to buy new, it means there is a lot of wastage.

“So where people are leasing, it is allowing them not only to make sure they’re up to date with the trends and things they want to follow, they’re able to make changes so they’re not attached to things longer and also they’re able to give it back – some of these things come with insurance so you don’t have to worry if things don’t go well. You don’t have to pay for the maintenance costs.

“Also, a lot of the time, because we can’t afford brand new, we tend to buy things that are much more second-hand and not as good quality.”

There are some words of caution when it comes to borrowing and leasing, however.

Mr Asuquo said people should not “just borrow from anywhere”, and should always take a look at the reviews.

He said: “Check the reviews and make sure that the quality is there.”

Looking at how to pay, and the terms and conditions is also important.

The financial expert said: “Make sure you look at what your rights are in regard to handing stuff back.

“It’s really important to know if you get something and it’s not of the qualify you want, how long you have to make up your mind if you want to keep it or send it back.

"Is there a returns policy? All of these types of things are really important to know, especially when you’re borrowing stuff.

“What are your rights? If it’s a long-term contract, when can you make a break? How much notice do you need to give to leave? It’s really important to know the terms and conditions and your terms and your rights."