The odds of winning in the Premium Bonds prize draw have improved to their best level since April 2008, now standing at 21,000 to one.

The prize fund was XYZ in the September 2023 draw, and there were XYZ winners.

Missing out on earning interest on savings each month isn’t for everyone, particularly amid banks and building societies increasing interest rates of late.

Laura Suter, head of personal finance at AJ Bell, said: “Taking a punt on Premium Bonds was a more attractive gamble when interest rates were rock bottom.

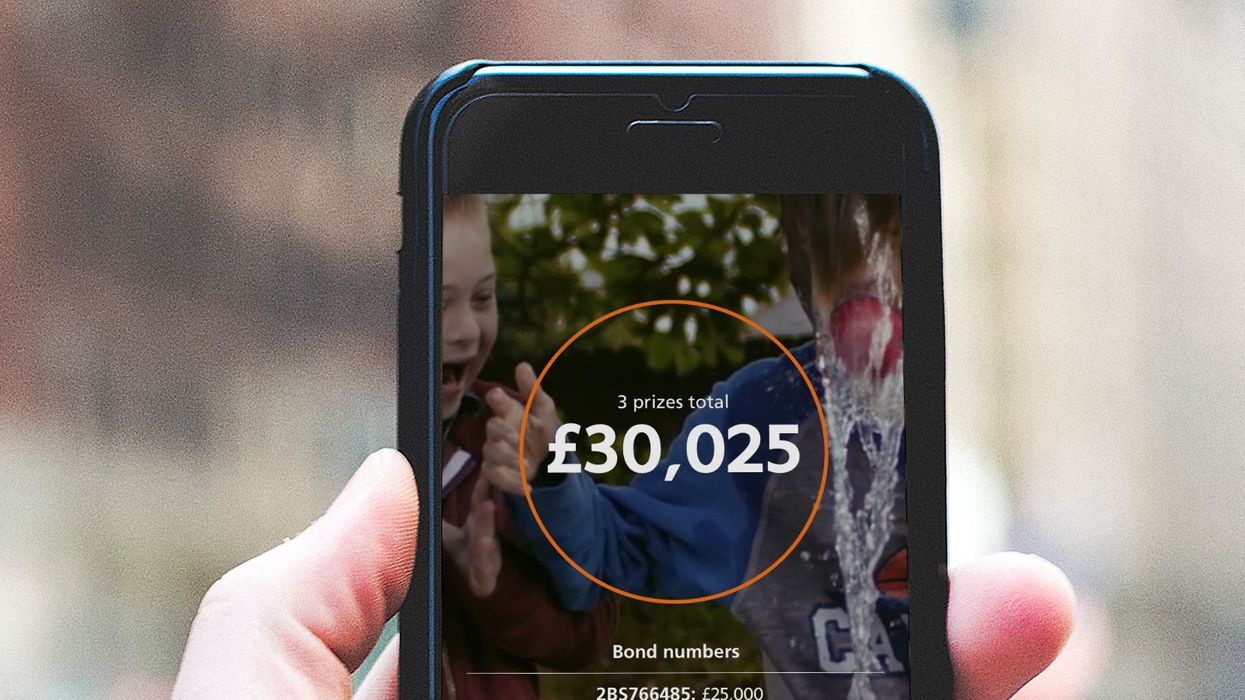

Premium Bonds savers now have an improved chance of winning a prize in the draw

|NS&I

“But now savers are giving up returns of five per cent on easy-access accounts for the chance they might win big on Ernie, which is a tougher call to make.”

For some, the risk of not winning anything in the prize draws is worth it, and there are several reasons why.

Among them may be the fact that prizes won in the Premium Bonds draw aren’t subject to tax.

Ms Suter explained: “Premium Bonds’ big selling point is that any money you win in prizes is tax free.”

While the Personal Savings Allowance means lots of people no longer pay tax on their savings income, improving interest rates being offered on savings accounts mean savers may face being taxed, unless they use an ISA or other tax-free savings vehicle.

Under the allowance, basic-rate taxpayers can earn £1,000 interest on their savings before they pay tax, while it’s £500 for higher-rate taxpayers.

Ms Suter said: “As interest rates have risen more people are hitting this allowance. Assuming their cash was in the current top-paying savings account earning five per cent, a basic-rate taxpayer would need to have £20,000 in savings to breach their tax-free allowance, while a higher-rate taxpayer would only need to have more than £10,000.

“On top of that, anyone who is in the highest rate tax bracket gets no savings allowance, and so will pay 45 per cent tax on any of their savings income.

“For these highest earners, or those who have already breached their allowance, the tax-free nature of Premium Bonds becomes far more attractive.”

The protection that comes with saving with NS&I is also a consideration for many risk-averse savers, although the Financial Services Compensation Scheme means a certain amount of money is kept safe.

“A big appeal of Premium Bonds is that they are run by the government, so they are seen as the safest-of-safe places to keep your money,” Ms Suter said.

“However, we’re all protected by the Financial Services Compensation Scheme, which covers up to £85,000 of money per person, per financial institution. This means that your money is theoretically as safe in any other bank with FSCS protection as it is with Premium Bonds.

“However, because NS&I is government run it can’t go bust, whereas a bank could go bust and then you’d have to reclaim your money through the compensation scheme. It’s a marginal difference but some people will feel much safer with their savings being with the government.”

LATEST DEVELOPMENTS:

Premium Bonds savers can check for prizes on the NS&I prize checker app

|NS&I

There’s no guarantee Premium Bonds savers will win a prize, but there is the chance of a significant savings boost – and some feel it’s worth entering the draw.

“For all those people who never win anything there will be someone who wins the top £1million prize,” Ms Suter said.

“If the savings rates on standard accounts still don’t excite you then you can gamble on winning one of the top Premium Bond prizes – after all, someone has to win it.

“However, anyone in this camp needs to be aware that they could win nothing, and so get no return on their money.

“Equally, your chances of winning depend on how much you hold in Premium Bonds. So, someone with £100 saved is much less likely to win than someone who has £20,000.”