Faced with rising borrowing costs and a £22billion "black hole" in the public finances, the Chancellor has suggested all options are on the table to cut spending.

If Rachel Reeves can tighten the purse strings while giving Britain's sluggish economy a shot in the arm, it would give her party its first success story.

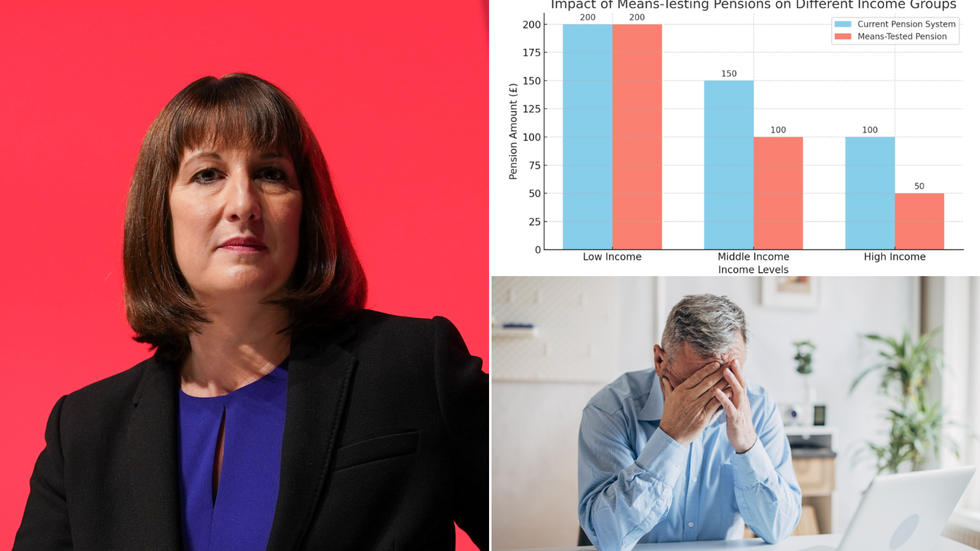

In theory, means-testing the state pension could do both. Labour can point to the success of the Australian model, which has been instrumental in keeping public pension outlays relatively low compared to other developed countries and has ensured pensions are primarily directed towards those in greater financial need.

However, the comparison is not perfect, as there are important differences between the two systems, and overhauling Britain's current arrangement is fraught with risk.

To understand why, GB News has interviewed industry experts.

Overhauling Britain's current arrangement is fraught with risk, not least for middle-income earners

|Getty Images/ChatGPT

But first, here's a primer on what means-testing means.

Means-testing for pensions or other benefits involves assessing an individual's financial situation to determine their eligibility for support and, often, the level of support they should receive.

In the UK, your national insurance (NI) contributions determine your eligibility for a state pension and the amount you'll receive, regardless of your other income or assets when you retire.

You need at least 10 years of NI contributions or credits to qualify for any state pension and 35 years for the full New State Pension, a flat-rate benefit to all eligible individuals based on their NI record, not their income or wealth in retirement.

Mean-testing pensions akin to the Australian model would mean retirement income from all sources (pensions, investments, earnings) would be assessed. Those with higher incomes might receive less or no state pension, regardless of how many NI contributions they've made.

The rationale is that it directs financial support to those who most need it while cutting back on public expenditure for those who do not.

However, such a move would be "highly politically and socially sensitive", says Mike Ambery, Retirement Savings Director at Standard Life, as Britain (unlike Australia), has a "lower level of minimum private pension contribution, so our dependency on the state pension is greater".

In the UK, the mandatory minimum contribution to private pensions (currently eight per cent of qualifying earnings, including employer and employee contributions) is significantly lower than Australia's planned 12 per cent superannuation contribution.

One of the perverse effects of means-testing could be to disproportionately affect those with modest private pension savings, who might not have enough from private sources to live comfortably without state support.

If the state pension is reduced or withdrawn due to means-testing, these individuals could face increased poverty in retirement.

LATEST MEMBERSHIP DEVELOPMENTS

Means-testing could disproportionately affect those with modest private pension savings

| GB NEWSSpeaking to GB News, Andrew Gosselin, a personal finance expert and Senior Contributor at Coupon Mister, made a similar point, noting that people who are just above the threshold for benefits can end up worse off than those who qualify, which feels "unfair and discourages saving".

He explained: "Middle-income earners, especially, might see no point in building up private savings if doing so means losing out on state support. It’s not just a hit to individuals—it’s a blow to the system’s credibility."

“It could also accelerate a planned increase to the state pension age," Ambery told GB News.

Currently 66, the state pension age is set to rise to 67 between 2026 and 2028 and a further increase to 68 is planned between 2044 and 2046.

If life expectancy increases over the coming years, and "twin pressures" of squeezed public finances and an ageing population continue, raising the state pension age higher and into the 70s will be an attractive solution, the retirement expert says.

"It would, however, be extremely unpopular and would disproportionately impact the poorest in society, who are most dependent on the state pension and often have shorter life expectancy," he added.

Then there's the logistics of implementing such a sweeping reform, which Gosselin calls a "logistical headache", adding: "Think of the sheer scale of assessing and re-assessing millions of people’s incomes and assets. It invites delays, errors, and plenty of frustration for retirees.

"Over time, the administrative costs can eat into the very savings the system is supposed to generate. While it might save money in the short term, the long-term effect could be that society is less prepared for retirement, which brings its own financial strain down the road."

Both experts agree that the pension reform is rooted in trying to address real issues, but it comes at a cost to individual financial security and trust in the system.

Gosselin concluded: "These changes might help on paper, but for the people relying on these pensions, they feel like a gamble. Retirement savings are about stability and predictability, and anything that undermines that creates a ripple effect of uncertainty."