Chancellor Reeves is considering an ‘Australian style’ means testing of the state pension in a bid to reduce the £137billion the Treasury spends annually on retirement pots.

Pensions are one of the UK government’s largest areas of expenditure, with two and half times more money being spent on supporting people in retirement than on defence.

As with the winter fuel allowance, Labour wants to claw some of this money back but faces heavy criticism for denying financial support to people who have worked and paid taxes all their lives.

An expert has confirmed the government is looking into adopting parts of Australia’s system of means testing the state pension by income and assets.

GB News has investigated Australia’s means testing system and can reveal it would have the following effects if rolled out across Britain.

Reduced pension for nearly all homeowners

Currently in Britain, the full state pension is £203.85 per week, based on 35 qualifying years of NI contributions.

There's no means test; everyone qualifying receives the same amount if they've made the required contributions, regardless of if they own their home and its value.

But in Australia, there are two major tests that decide how much of a pension you will receive.

They are the assets test and the income test.

The assets test links your pension with the value of your assets, namely your house.

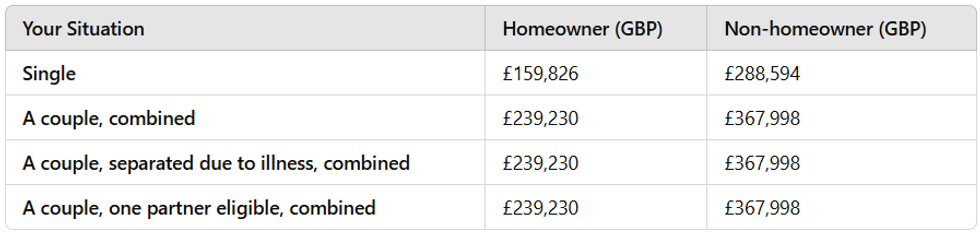

If your house exceeds a certain value, you are not eligible for a full state pension. The limits are as follows (thresholds have been converted to GBP using today’s exchange rate).

Asset value limits to qualify for state pension if Australia's pension system was adopted in Britain

|GBN/ChatGPT

Applying these limits to British pensioners would mean that if you are a single pensioner who owns a home worth over £160,000, your pension will reduce.

If you are married or in a relationship, that number rises to £240,000 before both of your pensions reduce.

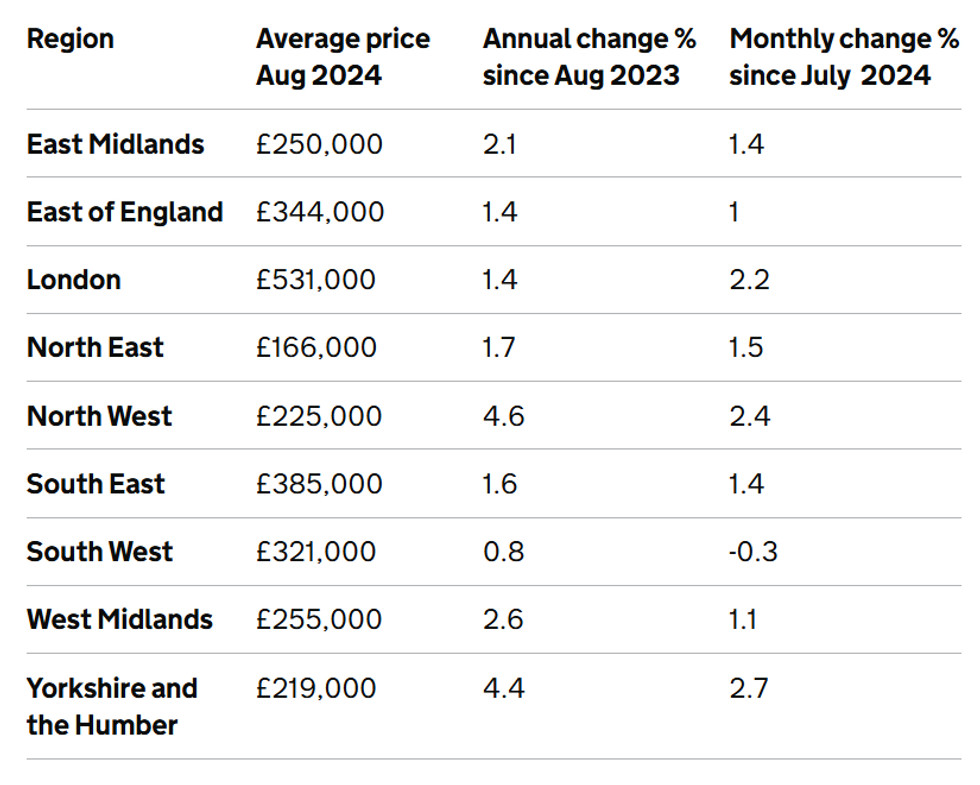

This will ring alarm bells for homeowning pensioners in Britain. The average price of a house in the UK rose to £293,000 according to latest government figures, well above the threshold in Australia where house prices are higher than Britain.

With homes worth £344,000 in the East of England, £385,000 in the South East and a whopping £531,000 in London, swathes of homeowning pensioners would see their state pension reduce if Australia’s system was adopted.

Average house prices in England

|Gov.UK

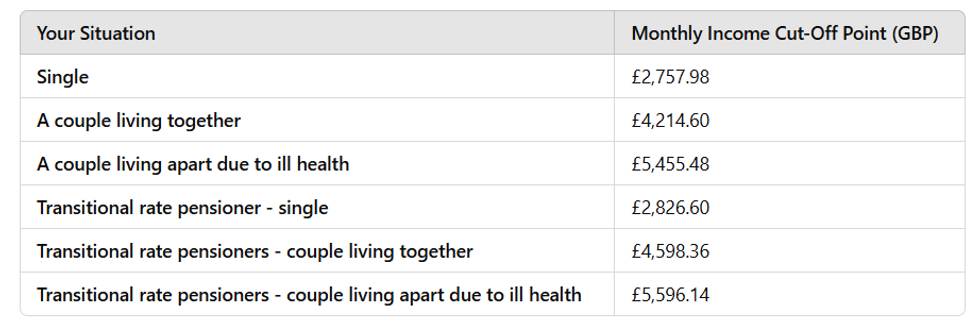

Reduced pension for earners on £36,000 per year

The income test links your pension with the amount you earn, including your savings, shares and super-annuation.

There are limits to how much you (and your partner) can earn to qualify for a full state pension. They are as follows.

Income limits to qualify for state pension if Australia's pension system was adopted in Britain

|GBN/ChatGPT

It means if the Australia style model was adopted in Britain, a single person earning over £2,757 would not receive any state pension support for that month.

For a couple, that rises to £4,214 per month.

According to Forbes, 60-year-olds in the UK make an average of £2772 per month, putting them just over the Australian style threshold.

That means the average 60-year-old earner in Britain would receive zero pension contributions on their salary from the government.

The potential measure comes as part of Labour’s sweeping pensions review launched in November aimed at tackling the retirement crisis in Britain.

Currently in Britain, workers aged between 22 and the state pension age earning at least £10,000 must be automatically enrolled into a workplace pension scheme.

Employers contribute at least three per cent of the worker's qualifying earnings, with employees contributing five per cent.

The full new state pension is £203.85 per week, based on 35 qualifying years of NI contributions.

There's no means test; everyone qualifying receives the same amount if they've made the required contributions.

Critics have consistently warned that this is not enough to live on, particularly if you have a mortgage.

It is worth noting in Australia, employers are required to pay 11.5 per cent of your salary into your pension pot, while the employee’s contribution is voluntary.

If this was adopted in Britain, experts have highlighted potential downsides, including the fact that increasing pensions costs for employers acts like another tax on hiring people.

This could lead to less job opportunities and lower wages as companies struggle under another financial burden.

This could be acute in Britain where Reeves has just slapped companies with a massive hike to Employers’ National Insurance Contributions.

LATEST FROM MEMBERSHIP:

Pensioners have reacted to No 10 refusing to rule out means testing pensions | GB NEWS / PARLIAMENT

Pensioners have reacted to No 10 refusing to rule out means testing pensions | GB NEWS / PARLIAMENTMeans testing could also disincentivise earning as higher wages means more money lost to the pension pot. This would only apply if paying into your pension pot was mandatory (which it is in the UK).

Means testing also involves accessing individuals’ personal finances to see whether they require state support.

If the individual is found to have sufficient means to live on, the state pension will not be available, meaning less money for retirement.

How high (or low) Labour would set the threshold remains to be seen, but the very act of accessing personal finances is likely to be unpopular, and almost certainly labour intensive and costly.

Mike Ambury, an insurer at Standard Life, outlined several benefits of the Australia system, namely the fact less affluent working Brits will receive larger pensions pots and the Treasury will save millions.

However, the expert also highlighted why it might not work in the UK. He said: “It may produce a cost saving [to the Treasury] but, equally, the administration process of applying is very labour-burdened, as evidenced in Australia.

“Means-testing and an administrative-heavy application process would [also] be a real issue for UK retirees.”

A government spokesperson said: "Our commitment to the Triple Lock is unwavering because we want pensioners to enjoy the dignity and respect they deserve in retirement.

"This means millions will see their State Pension rise by up to £1,900 over this parliament.”

The next stage of Reeves’ pensions review has been postponed indefinitely.