Britons are being urged to use three simple pension savings hacks to boost their retirement income by £243,200, according to new analysis from interactive investor.

This research comes after the state pension rose by 4.1 per cent last week but the investment platform is questioning how "comfortable" an income the retirement benefit provides.

Under the triple lock, the full state pension has increased by £470 to £11,973 a year, but analysts claim it still falls short of what is needed for a basic retirement income.

Interactive investor emphasises that relying solely on the state pension won't provide a comfortable retirement, highlighting the importance of additional pension strategies.

Pensioners could get a significant boost to their retirement income thanks to three savings hacks

GETTY

The first recommended pension savings strategy involves seeking employment with companies offering more generous pension contributions.

Moving to an employer that pays five per cent into your pension rather than the minimum three per cent could boost someone's retirement savings by £116,700, assuming you earn £35,000.

This figure increases substantially for higher earners - to £197,700 for those on £60,000 and £328,200 for those earning £100,000. Notably, this simple job-switching strategy requires no additional personal contribution.

Furthermore, the second strategy utilises salary sacrifice for pension contributions, allowing employees to save money on National Insurance.

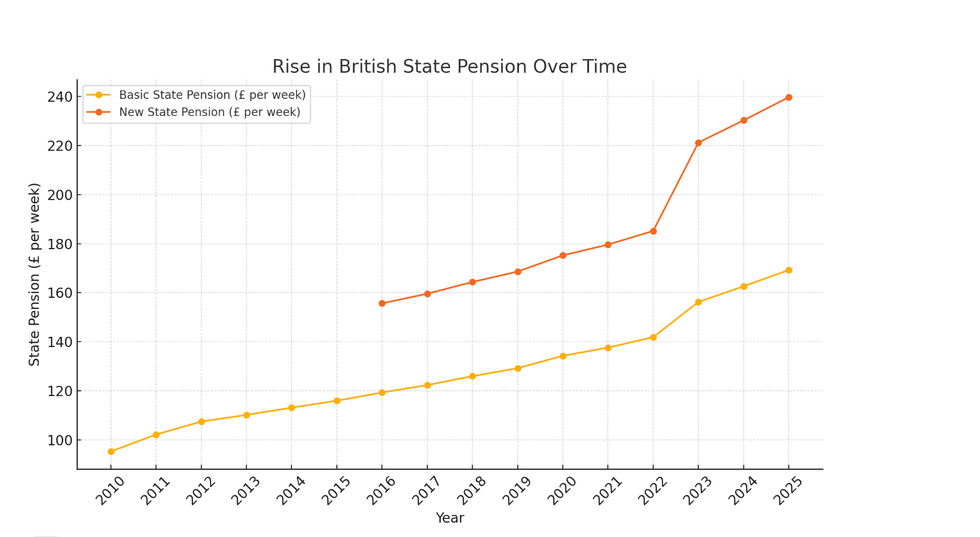

The rise in the British State Pension over time, including the 4.1 per cent increase in 2025

ChatGPTBy reinvesting these tax savings into a Self-Invested Personal Pension (SIPP) or workplace pension, retirement wealth could increase by between £15,800 and £27,700.

This approach effectively turns tax that would otherwise go to HM Revenue and Customs (HMRC) into additional individual retirement savings.

Finally, the third strategy suggested by interactive investor involves investing a portion of any pay rise directly into someone's pension pot.

Setting aside just £50 from a salary increase and putting it into a SIPP or workplace pension could boost their retirement wealth by £98,900 by retirement.

Britons are being warned the state pension could look different once they reach retirement GETTY

Britons are being warned the state pension could look different once they reach retirement GETTY According to analysts, this approach allows individuals to increase their pension contributions without feeling the pinch in their monthly budget.

These three strategies combined could raise the pension wealth for a worker on the average salary of £35,000 to around £243,200, according to interactive investor.

Camilla Esmund, a senior manager at the firm, outlined how these proposals are designed to help everyday Britons; not just the country's super rich.

She shared: "It's encouraging that you don't need to be a high earner to add substantial sums to your pension with some modest tweaks.

"Taking simple steps like filling in salary sacrifice forms or checking employer contributions when you move jobs could boost your pension significantly over your working life."

Interactive investor also urges pension savers to "dare to compare" their fees, launching a new comparison tool to help identify potential savings.

LATEST DEVELOPMENTS:

Britons are being encouraged to change jobs to bolster their retirement income

GETTYOver decades, excessive charges can significantly reduce individual retirement funds by tens of thousands of pounds if savers do not take action.

"It can be disheartening to integrate good habits, stick to your investment strategy for the long term and see the fruits of compounding take effect over time, only for your growing pot to be eaten away in unnecessary fees," explains Esmund.

Esmund added: "Not everyone is in a position to move jobs, but when the time comes, it’s vital to find out more about the pension. It forms a crucial part of your pay package and varies significantly between employers - some pay in just three per cent while others pay up to 15 per cent.

"Over years of work that could add thousands to your pension wealth and make the difference between a basic and more comfortable retirement."