Millions of UK homeowners are being urged to lock in sub-four per cent mortgage deals as an estimated 1.8 million face steep payment increases when their fixed rates expire this year.

Homeowners who secured mortgages in 2020 could see their monthly payments surge by 31 per cent when remortgaging in 2025, new research has found.

The average homeowner is set to pay an additional £3,273 per year as mortgage rates have climbed significantly since the pandemic-era lows, according to My Home Move Conveyancing.

The warning comes as those who locked in historically low rates during 2020, when average rates were just 2.4 per cent, now face rates around 4.77 per cent for five-year fixes.

Major banks have started slashing mortgage rates below the crucial four per cent mark, offering a window of opportunity for homeowners facing renewals.

Santander became the first major lender this year to break the four per cent barrier, launching new two- and five-year fixed deals at 3.99 per cent for borrowers with a 60 per cent LTV.

Homeowners who secured mortgages in 2020 could see their monthly payments surge by 31 per cent when remortgaging in 2025

GETTYBarclays is following suit, announcing rate reductions below four per cent across its residential purchase and remortgage products from February 13.

NatWest has also joined the rate-cutting trend, reducing rates by up to 36 basis points on remortgages and up to 16 basis points on purchases, including high-value and green mortgages.

The average homeowner could face a £272 increase in monthly mortgage payments, equating to £3,273 annually when switching to new deals.

Those opting for shorter two-year fixed rates could see even steeper rises, with payments potentially increasing by 31.5 per cent compared to their current deals.

In 2020 the average mortgage rate was around 2.4 per cent, whereas now, those remortgage face average rates around 4.77 per cent for five-year fixes and 4.98 per cent for two-year terms.

LATEST DEVELOPMENTS:

The calculations from are based on a typical 20 per cent deposit with 30-year repayment terms, according to My Home Move Conveyancing's nationwide study.

The impact varies significantly across regions, with London and the South facing the steepest increases in mortgage payments.

Homeowners in Kensington and Chelsea and the City of Westminster are bracing for the highest rises, with annual mortgage payments projected to increase by over £13,000.

Other London boroughs including Camden, Richmond upon Thames, Hackney, and Barnet will see monthly payment increases ranging from £486 to £830. St Albans, Surrey, and Cambridge residents face monthly rises exceeding £427.

In contrast, northern regions like Burnley, Durham, and Blackpool will see more modest increases, with projected monthly rises between £84 and £105 for 2020 buyers.

Alistair Singer, director at My Home Move Conveyancing, explained the dramatic market shifts since 2020.

He said: "Since 2020, the property market has undergone substantial shifts. In response to the pandemic, the Bank of England slashed its base rate to 0.1 per cent, resulting in some of the most affordable mortgage rates in years.

"Many homeowners secured fixed-rate deals during this time, while the governments stamp duty holiday further incentivised property purchases.

"However, as these five-year deals come to an end, the mortgage landscape looks very different, and some may choose shorter-term fixed rates, hoping that the base rate will come down further in the next couple of years."

Singer emphasised the importance of early planning for remortgaging, urging homeowners to understand their finances thoroughly.

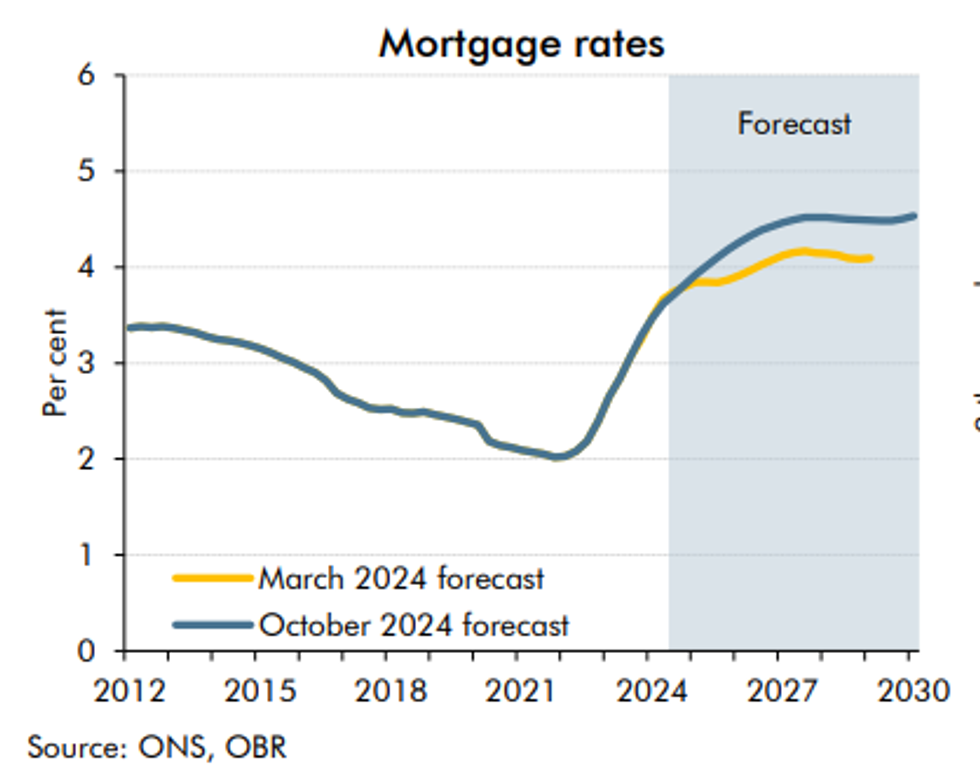

Mortgage ratesOBR

Mortgage ratesOBRHe explained the key to remortgaging is to start planning early. Having a deep understanding of one's finances can help them act on a good deal quicker.

Homeowners approaching the end of their fixed rates should check their current interest rate, expiry date, and remaining mortgage balance.

Those considering switching lenders should review their contract terms, including early repayment charges and exit fees.

Essential documents for remortgaging include proof of income, recent bank statements, and ID, with Singer recommending consultation with mortgage brokers or conveyancers for guidance.