Around 50,000 UK households are facing a significant financial month this month due to a "ticking mortgage timebomb" as their five-year fixed-rate deals from February 2020 come to an end.

Analysts are warning that tens of thousands of British homeowners will see their monthly payments surgehomeowners will see their monthly payments surge by more than £280 when they are forced to remortgage at current rates.

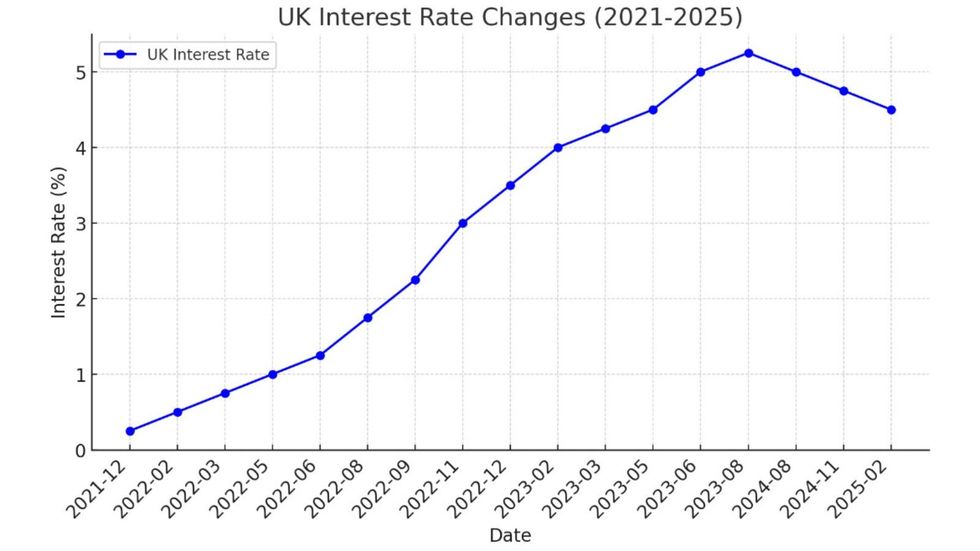

The increase comes despite today's Bank of England decision to cut interest rates to 4.5 per cent, as affected households move from their deals that offered much lower rates.

Analysis by household money-saving tool Nous.co shows households coming off five-year fixed mortgages will see their rates jump from 1.88 per cent to 4.5 per cent.

Do you have a money story you’d like to share? Get in touch by emailing money@gbnews.uk.

Experts are worried about the looming mortgage "timebomb"

|GETTY

For a typical £200,000 mortgage over 25 years, monthly repayments will rise from £836.07 to £1,111.66 and compound existing financial pressures amid the cost of living crisis.

This represents an increase of £283.29 per month, or £3,399.53 per year, for affected homeowners and suggests the Bank of England's latest efforts will come too late for those looking to remortgage.

Greg Marsh, the CEO of Nous, issued a stark warning: "Falling interest rates are welcome news for mortgage holders. But the UK's mortgage timebomb hasn't fully exploded."

"Millions of households are still on mortgage rates below three per cent and will see their monthly payments soar when they refinance over the next three years," he added.

LATEST DEVELOPMENTS:

Mortgage payments are expected to rise for those coming to an end of their fixed-rate term

| GETTY"In February alone, 50,000 households are coming off five-year mortgages and facing painfully high rates for the first time. A typical household will see their payments rise by nearly £300 a month. After years of soaring prices, many will struggle to manage."

Mark Ashbridge, the managing director of Ashbridge Partners, broke down who are the likely winners of the base rate cut when it comes to navigating the UK property market.

He said: "What does this mean for those looking to buy and if you’re one of 1.8 million people that have a mortgage maturing in 2025? We’d expect the banks to cautiously offer some new products in the coming weeks.

"However, these will largely be aimed at the lower loan-to-value applicants, those on 60% - 70 per cent, as well as first time buyers, which could see more products with a higher loan-to-income ratio aimed towards them.

“Those people approaching the end of their mortgage product term and new buyers will want to remain vigilant over the coming weeks to see how the banks react."

"For example, we’ve seen some fairly material peaks and troughs in five-year fixed rates offered over the past 12 months, which can have a real impact on your affordability.

"It’s therefore likely that better mortgage deals will arrive shortly and you will need your mortgage advisor primed and ready to secure these.”

The central bank has made multiple changes to the base rate

Alice Haine, a personal finance analyst at Bestinvest by Evelyn Partners, emphasised the predicament many households approaching the end of their fixed-rate mortage.

She shared: "Those nearing the end of their product’s fixed-rate term now have a difficult decision on their hands; do they secure another fixed-rate deal or take a punt on further interest rate cuts, which could mean a tracker might work out best over the longer term?

"Seeking advice from an independent mortgage broker - who can scour the market for the most cost-effective solution for an individual’s circumstances – and getting a deal in place is key to avoid reverting to a lender’s ultra-expensive standard variable rate."

The Bank of England's next MPC meeting is scheduled to take place on Thursday, March 20, 2025.