Homeowners may be paying a “shocking” £3,000 more in mortgage repayments due to a simple mistake, experts claim.

Nearly a third of households (31 per cent) let their mortgage fall into a higher rate for at least one month after their fixed rate deal ended, according to new research by Finder.

The total period of time during which people allowed their mortgage to revert to a higher rate was 10 months on average over the course of their deal, the survey found.

An individual paying off the cost of the UK’s average house, worth £281,913, on a competitive fixed 5.5 per cent three-year rate would pay £1,361 per month during this period.

However, if that same person did not remortgage immediately at the end of the initial fixed term, the interest rate would revert to the lender’s standard variable rate.

Currently, this is usually around 7.5 per cent for homeowners.

Do you have a money story you’d like to share? Get in touch by emailing money@gbnews.uk.

Homeowners are being warned about a "shocking" mortgage mistake

|GETTY

As a result, this would cost the homeowner around £1,661 per month, which is an extra £300.

The average person paying 10 months of this would therefore lose an extra £3,000 to pay the extra interest.

Around 11 per cent of respondents who had been on a revert rate said they had paid this higher amount for more than one year.

Some three per cent admitted to paying a revert rate for more than five years, which means an extra £30,000 in interest costs, analysis suggests.

Liz Edwards, a mortgage expert at finder.com, urged homeowners to check their deal to avoid being saddled with these mounting bills.

She explained: “It’s easy to let renewals slide for a while and even if you remember to renew your mortgage, if you leave it too late then you may need to wait a month or two for the rate on your new deal to kick in.

“For mortgages this can have a huge impact on the amount you pay.

“The extra monthly cost is shocking in itself but as an illustrative point, if someone paid off a 30-year mortgage using the current average revert rate vs the current average 3-year rate, they’d pay an extra £180,000 in needless interest.

“So, set a calendar reminder and make sure you find a new deal in plenty of time before your fixed-deal expires.”

In recent years, homeowners have been forced to pay rising mortgage bills due to mortgage rate hikes.

LATEST DEVELOPMENTS:

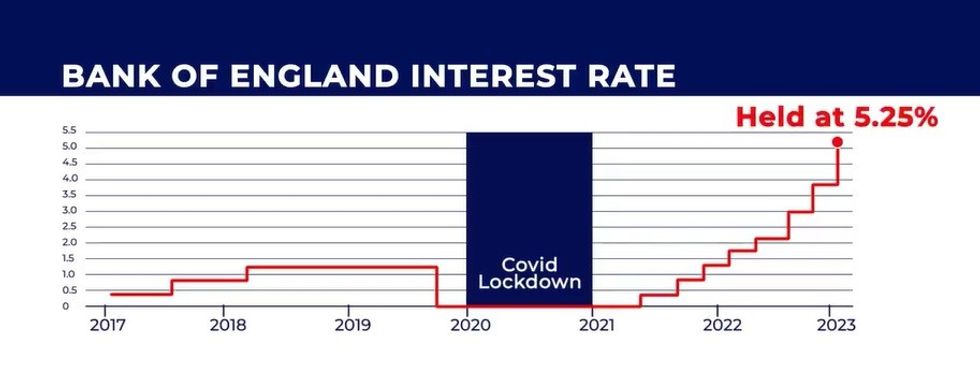

The Bank of England has held the base rate at 5.25 per cent in recent months | GB NEWS

The Bank of England has held the base rate at 5.25 per cent in recent months | GB NEWSThis followed the Bank of England’s decision to raise the base rate in its fight against inflation.

With the Consumer Price Index (CPI) rate of inflation falling below four per cent, it is expected a rate cut from the central bank is on the cards.

As it stands, the Bank's base rate has been held at 5.25 per cent since August 2023.

However, analysts have warned that this is unlikely to happen until the later half of 2024.