A man who spent almost 20 years planning and preparing for later life says his retirement income is "just going down the toilet" following the Bank of England's 14 consecutive hikes to the base rate.

"The interest rates have gone up at such a speed that you can't really keep up with it," John, 63, whose name has been changed, said.

John first became a landlord 18 years ago, after seeing friends "turning over a lot of money" with buy-to-lets.

Within six months, he bought a second property.

"The first two did really well," he told GB News, explaining he had got the homes revalued and remortgaged in the first year.

He soon expanded his buy-to-let portfolio, at one point holding five different properties in the north of England.

"I went under the logic of 'what's the least risk?' So I bought everything in a more affordable area, rather than one more expensive property. Because if you have one property and you lose a tenant, you've got big trouble," he said.

"By spreading it over five properties, I was able to cover shortfalls for a long period of time."

Have you got a money story you'd like to share? Get in touch by emailing money@gbnews.uk.

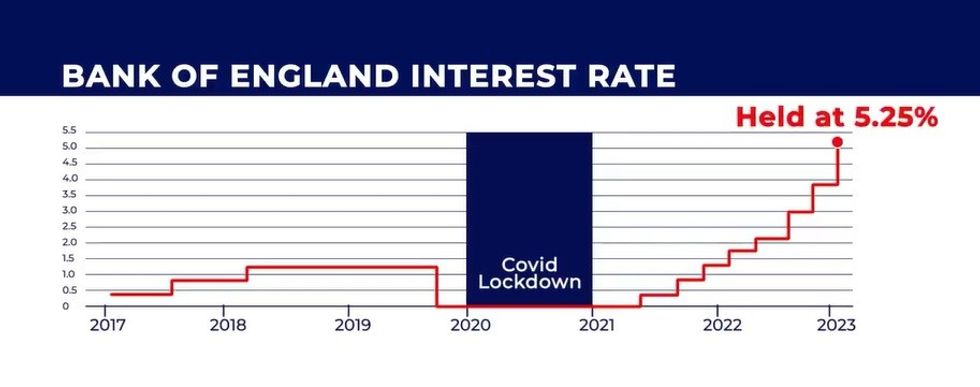

The Bank of England base rate has held interest rates at a 16-year high since it was hiked to 5.25 per cent last August

|GB NEWS

John, who is now an expat living in Europe, first started to experience financial problems last year, as his mortgage rates surged to “ridiculous” levels.

Being self-employed, he had already been "a bit knocked over" financially, having been unable to work during the Covid years.

As the Bank of England base rate increased - it was hiked from 0.1 per cent in December 2021 and has stoof at a 15-year high of 5.25 per cent since August 2023 - John had to shell out more and more each month on his mortgages, which were trackers of 1.5 per cent above the base rate.

Things had been "tight" for John anyway, and he had been saving up to fix a severe damp problem in one of the properties, which he had stopped letting out until the issue was resolved.

"I'd had some bad luck," he said. "We had put quite a lot of money in over the years, but it still kept coming up."

John was saving up for the repair work, which would have cost around £10,000.

"Things were tight anyway, so the money I was trying to save up to have this house redone ended up being put into prop up the mortgages.

"Over the years, the base rate had remained very, very low, which had meant I'd managed to be able to carry the one with the damp problem fine - even though it had no tenant in it for a couple of years, and I was paying obscene council tax on it."

John tried to seek help from his local council so he could pay for the work and let the property out again but to no avail.

He said: "They send you to pillar to post.

"Everyone is complaining there's not enough property, that we've got a property crisis, but everyone's prepared to kick the landlords down. Landlords get really bad rights."

John's average mortgage repayment had been around £130 per month, but within a year, it had shot up to £400 per month.

He said: "I got to the point where things weren't covering themselves. In all my years, I've never had negative credit at all, ever.

"I wasn't making amazing amounts of money before, but enough to cover repairs and things.

"It rang along nicely for 15-odd years without a problem. If a property became empty for a short period, say six months, the whole thing would still carry itself. But the interest rates came so fast, so quick, I thought I'd have to get out of this one."

John has now had to surrender four of his houses, which had been meant to support him in retirement, to the mortgage company.

"I said to them, 'Were I to actually have a better rate, we could get out of this problem.' But although they put it under review, they are not interested," he said.

"This is a typical case of the banks making hay while the sun is shining, on the backs of everyone else. They are not showing a great deal of sympathy whatsoever.

"I propped it up as long as I could. I've put myself into a bit of debt due to it. I said, 'I can't carry on doing this. If we carry on doing this, we're going to be completely down the pan."

Unfortunately, some of his properties have not been looked after by the tenants as well as he'd hoped, meaning their values were "not really what they should have been".

To "cover his back", John decided to sell his "best" property, in the hopes the capital could help him make ends meet.

Selling his final buy-to-let is proving more difficult than he'd expected. John said: "It's not a seller's market at the moment because there's so much unsureness of the interest rates."

John thinks the 14 consecutive interest rate hikes were "totally unnecessary".

He said: "I don't know how anybody is going to survive if they've got a mortgage for a £400,000 house, who comes off a fixed rate of maybe two or three per cent and goes onto five, six or seven per cent."

LATEST DEVELOPMENTS:

The mortgage on John's remaining property, which is up for sale, is with another lender, who he says has been "far more considerate".

He added: "They have been completely different; they've been very communicative, although they don't want to reduce the interest rate."

John pointed out that, in his experience, landlords don't necessarily make as much money on buy-to-lets as people may assume.

"After I have paid for the mortgage and property insurance, I have £26 left," he said, pointing out he also needs to save money for repairs.

On some of the properties which have now been repossessed, mortgage rate hikes meant the rental income no longer covered the costs.

“After the agent’s fees, insurance, and everything else, I was looking at a £1,000 a month deficit. I can’t keep up with that for very long - I earn a reasonable living but I’m not a millionaire.”

The properties were intended to support him in retirement. "At 63, my pension is just going down the toilet after nearly 20 years of surviving fine in the buy-to-let market," John said.

"I'm going to have to work for a lot longer, now. I've got a bit of a pension, but it's going to be a lot tighter than it was without a doubt.

"I put in a 15 per cent cash deposit into each property myself, and I'm probably not going to see that because the properties that have been returned to the lender will more than likely be sold off at auction. I'll be lucky if they cover their own costs. I don't see myself getting much of a profit out of it. If there's any shortfall, I'm responsible for that.

“If I’d seen things slowly going up, I could have done something about it. But you don’t expect things to go up that fast.”

John feels sympathy for the knock-on effect for renters. He said: “A lot of people who rent are getting in the neck now because the landlords have no choice but to put up the rent.”