The Bank of England is being urged to take action over interest rates as soon as possible as 4,000 homeowners face "shock" hikes to their mortgage repayments every year.

High street lenders have raised mortgage rates in response to the central bank increasing the base rate with thousands of families on fixed-rate deals at risk of paying more in 2024.

Ahead of the central bank's Monetary Policy Committee (MPC) meeting on August 1, experts from TotallyMoney are breaking down the devastating impact hiked mortgages are having on peoples' finances.

According to the financial institution, more than 4,000 homeowners face a new "financial shock "when their current rate mortgage comes to an end at some point this year.

A consequence of the Bank of England's decision-making in regards to the base rate is that households are being forced to contend with higher interest payments.

For context, the average-five year fixed mortgage came to 1.70 per cent and now sits at 5.49 per cent.

Do you have a money story you’d like to share? Get in touch by emailing money@gbnews.uk.

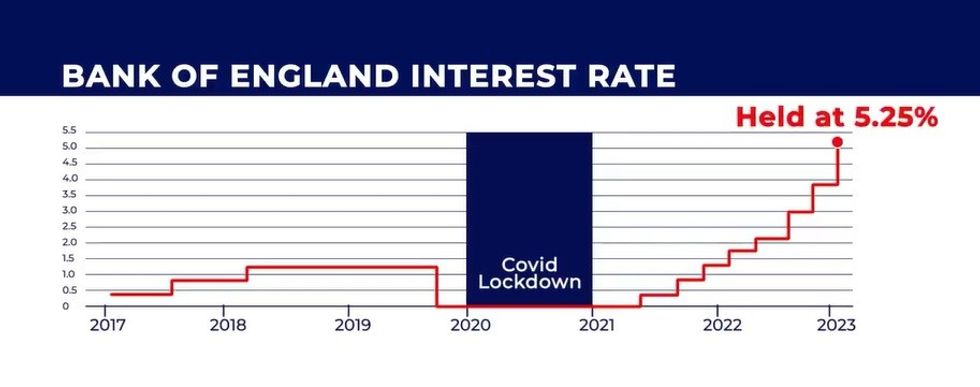

The Bank of England base rate has held interest rates at a 16-year high since it was hiked to 5.25 per cent last August | GB NEWS

The Bank of England base rate has held interest rates at a 16-year high since it was hiked to 5.25 per cent last August | GB NEWSExperts are sounding the alarm that those who do not secure a cheap new deal face will be placed onto their bank or building society's standard variable rate (SVR).

Currently, the average SVR is sitting at 7.5 per cent with some high street lenders charging as much as 9,24 per cent.

Britons making repayments on the average home would previously have been paying £714 per month in mortgage repayments before the recent rate hikes.

However, the same household would now pay £1,004 on the average two-year fixed deal which is £3,480 more per year.

Furthermore, families face paying £956 if they are on the average five-year fix and £1,121 on the average SVR, which comes to £2,904 and £4,884 per year.

Based on TotallyMoney's analysis, mortgage arrears cases are projected to rise from 105,600 in 2023, to 128,800 by the end of 2024.

Currently, the Bank of England has raised the base rate to 5.25 per cent and has held it at this level since August 2024.

Analysts are pricing in a rate cut in the later half of the year but some are suggesting it could take place as early as this week.

Alastair Douglas, the CEO of TotallyMoney, outlined what homeowners should be doing to prevent their mortgage bills from skyrocketing even further.

He explained: "Every day, more than 4,000 homeowners face a fresh financial shock when their existing cheap mortgage offer comes to an end.

LATEST DEVELOPMENTS:

Interest rate hikes have pushed up mortgage repayments for many | GETTY

Interest rate hikes have pushed up mortgage repayments for many | GETTY "The options are then; lock in a new deal, paying almost double the interest rate, and potentially incurring product fees of £1,000 — or move onto the SVR, which can be as high as 9.49 per cent.

"So double-check when your existing deal is ending, and make a note to start looking for a new one in advance. You might even be able to lock in a new offer up to six months in advance.

"You should also keep an eye on your credit report, as banks will usually reserve the best offers for those with the best scores.

"It’s free to do, and you’ll see the same information they use when choosing who to lend money to. If you spot any errors you can raise a dispute, and by checking your credit report you can make sure the information is correct and up to date."