Savers are rushing to raid their pensions early in an effort to beat Chancellor Reeves ‘triple tax hit’, advisors have revealed.

Withdrawing money from a pension early can mean it is treated as income and taxed accordingly, but this hasn’t stopped some from incurring income tax bills of up to £20,000 to avoid Reeves’ drastic reforms pension rules.

Reeves’ reforms include subjecting pensions to inheritance tax from 2027, a controversial measure that has been labelled ‘anti-aspiration’, ‘anti-wealth’ and ‘unfair’ as the income has already been taxed when it was earned.

The other prongs of the ‘triple hit’ include the fact beneficiaries of those who die over the age of 75 will also have to pay income tax at their marginal rate when they withdraw the inherited pension savings.

Lastly, those passing on more than £2million will lose the main residence relief at a rate of £1 for every £2 over the threshold, meaning the whole allowance is lost once the estate is worth over £2.35m.

It means some grieving families who don’t plan astutely will be taxed at 90 per cent, accountancy firm RSM has warned.

As a result, people are withdrawing large sums of money from their pensions and accepting the income tax hit.

Nick Nesbitt, of accounting firm Forvis Mazars, said: “Lots of clients who were looking to save their pension before the Budget are now drawing more income out and accepting higher tax bills.

“The strategy previously was to limit withdrawals to £50,000 a year so you are only paying a marginal rate of 20pc. But people are now raising the yearly income to £100,000 and taking the 40pc tax hit.”

Rachel Reeves is subjecting pensions to IHT

PAIt means for someone moving from withdrawing £50,000 from their pension to £100,000 in one year can expect to see their tax bill increase by around £20,000.

Even with the increased tax bill, this could be a prudent move, particularly for pensioners in poor health who might die and see their pension raided by the Treasury.

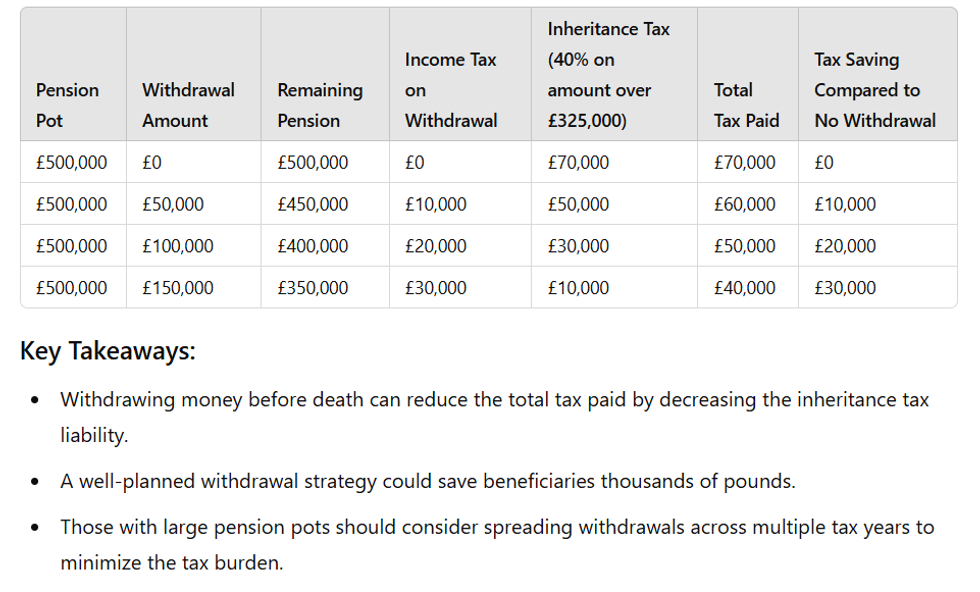

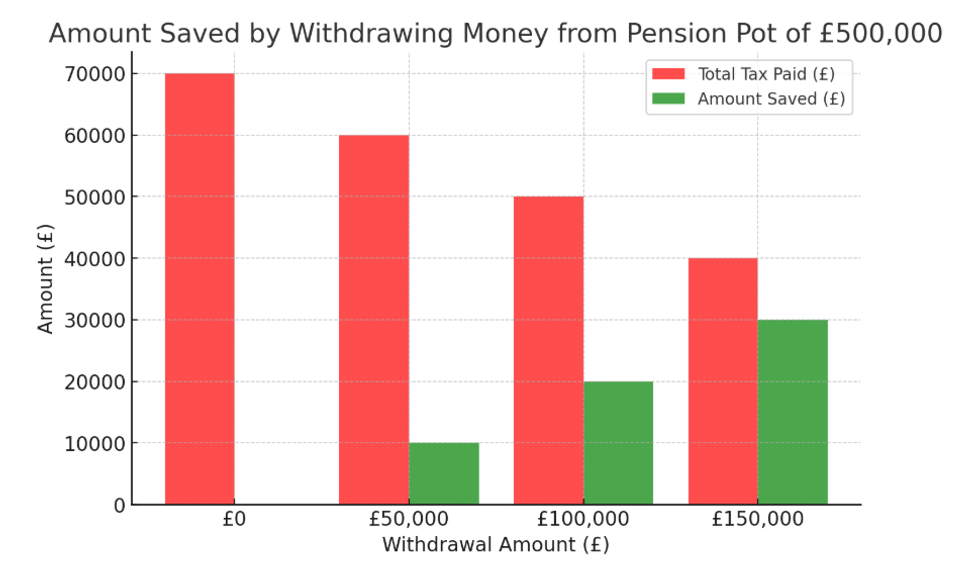

For example, if someone had £500,000 in their pension pot, they would pay £70,000 to the taxman when they die in IHT (40 per cent of amount over nil-rate band of £325,000).

If they withdrew the £100,000 (leaving them with £400,000 in the pot), took the £20,000 income tax hit and then died, that would result in an inheritance tax bill of £30,000 (40 per cent of amount over nil rate band).

Adding the income tax bill (£20,000) and the inheritance tax bill (£30,000) equals £50,000, £20,000 less than if the person had died without making the withdrawal.

If we change the amount someone withdraws from their pension, we can see how their total tax bills (income plus IHT) changes.

How much you could save by withdrawing money from your pension

How much you could save by withdrawing money from your pension

GBN

How much you could save by withdrawing money from your pension

How much you could save by withdrawing money from your pension

GBN

For someone withdrawing £150,000 (£30,000 income tax bill), if they died their reduced pot of £350,000 would only incur IHT on the £25,000 over the nil rate band (£10,000).

Adding £30,000 and £10,000 equals £40,000 total tax bill, £30,000 less than if the person had made no withdrawal and then died and incurred IHT bill of £70,000.

Jason Hollands, of wealth manager Evelyn Partners, said: “You’ve got to take into account the post-tax impact when you withdraw pension savings, that’s important to consider. Some people will be taking tax-free cash, some people are increasing their withdrawal rate.

“Age and health need to be considered when deciding how much to take out. If you’re healthy, basically, you have longer to extract money.”

The Treasury was approached for comment.