Inflation increased by four per cent in the year to January 2024, remaining flat compared to the previous month.

The Consumer Price Index (CPI) remained flat compared to the previous month, defying experts' forecasts, who had expected inflation to tick up slightly.

Inflation increased by four per cent in the year to December 2023 - the first rate increase since February last year.

Speaking on GB News this morning, Liam Halligan said: "Most of us thought that inflation would tick up slightly. The general trend is down - inflation was up at 11 per cent back in October 2022. It's now down at four per cent.

The UK rate of inflation remained unchanged at four per cent in January 2024

GETTY

"It doesn't mean prices are flat - no way. Everyone who goes to the shops will tell you that. It means that in January last month, prices, if you indexed together all prices into one measure, prices on average were four per cent higher in January 2024 than they were in January 2023."

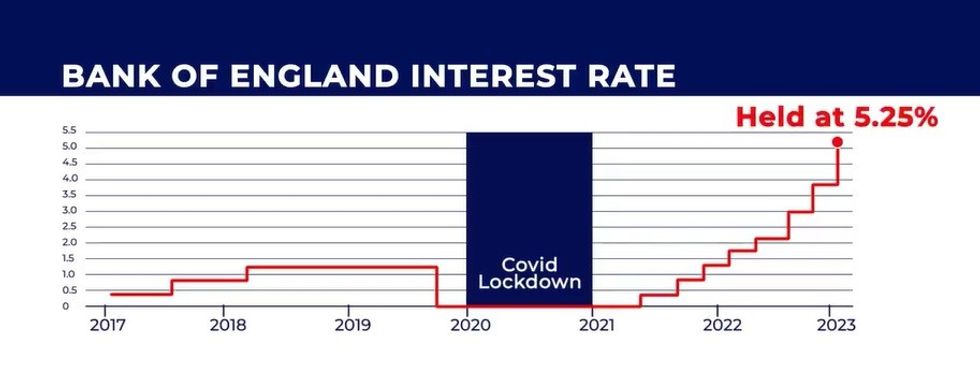

Turning to interest rates, Mr Halligan said it's unlikely the Bank of England would cut the base rate next month, given the figures.

He said: "I think when inflation is flatlining and not going down, it's very very difficult for the Bank of England to lower interest rates. I think interest rates will stay at 5.25 per cent, the base rate, in March.

"The first sign that they could possibly come down is April, but possibly May," Mr Halligan predicted. "Of course mortgage rates are already coming down in anticipation because they reflect future interest rates from the Bank of England."

Chancellor Jeremy Hunt said: “Inflation never falls in a perfect straight line, but the plan is working; we have made huge progress in bringing inflation down from 11 per cent, and the Bank of England forecast that it will fall to around two per cent in a matter of months.”

However, critics have said Mr Hunt and Prime Minister Rishi Sunak were premature on celebrating the easing of inflation last year.

Lily Megson, Policy Director at My Pension Expert said: “Late last year, the Prime Minister celebrated reaching his 5 per cent inflation target. We were told this was a victory, but the reality was that Britons were still grappling with the repercussions of 18 months of soaring inflation.

"Now, months later, with inflation still at four per cent, we can see how premature the government’s back-slapping was – and it’s not good enough."

Ms Megson warned long-term financial planning and preparing for retirement has become "a minefield" as inflation continues to diminish the real-terms value of people's pension pots.

“More help is desperately needed," she said. "It’s crucial going forward that the government ramps up its support to those struggling with their finances and their financial planning.”

Alice Haine, Personal Finance Analyst at Bestinvest by Evelyn Partners, said despite being lower than expected, inflation remains "worrying" for households hoping to see the back of the cost of living crisis.

She added: "The latest inflation data may also be a blow for mortgage holders and prospective buyers desperately hoping for interest rate cuts.

"Borrowing costs remain high relative to the pre-tightening cycle instigated by the Bank of England in December 2021, but the good news is that fixed mortgage rates have eased significantly from their peak last summer.

LATEST DEVELOPMENTS:

The Bank of England has held the base rate at 5.25 per cent in recent months

GB NEWS

"The latest inflation data may also be a blow for mortgage holders and prospective buyers desperately hoping for interest rate cuts.

"Borrowing costs remain high relative to the pre-tightening cycle instigated by the BoE in December 2021, but the good news is that fixed mortgage rates have eased significantly from their peak last summer."

Alastair Douglas, CEO of TotallyMoney said while inflation may be "far below" the 11 per cent peak seen in late 2022, the impact "will be felt for years to come".

He added: "The cost of living is now considerably higher than it was, and the poorest households have been hit the hardest.

“Savings have been spent, and the government is barely supporting those it’s supposed to serve. For 11 million people, borrowing is now the only option — but many mainstream lenders are choosing not to lend to those who need it the most.

“Unregulated borrowing is soaring, meaning many are turning to buy now pay later, payday loans and illegal money lenders — falling off the radar and papering over the cracks of what in reality is a financial crisis.

“So while the headline numbers may say inflation is low, or unemployment is steady, the reality is that millions of people are struggling to keep up, more than half a million UK businesses are in significant financial distress, and nobody is receiving the levels of support they need to survive.”