Inflation has fallen to two per cent in a major win for Britain's economy, according to the latest figures from the Office for National Statistics (ONS). However, experts are warning the Bank of England is "unlikely to be satisfied" with cuts to interest rates expected to not take place until later in the year.

The consumer price index (CPI) rate for the 12 months to May 2024 eased from 2.3 per cent to the Bank of England's desired target for inflation.

This comes after Prime Minister Rishi Sunak, who is in the middle of the General Election campaign, pledged to bring the CPI rate down to two per cent.

Prior to today, the majority of analysts forecast inflation dropping to this level which would represent the first time it has been at the Bank's target since July 2021.

Britons have been forced to contend with inflation-hiked prices for goods and services amid the ongoing cost of living crisis.

Despite this drop, experts are reminding the public they will have to wait longer for an interest rate cut from the Bank of England.

Do you have a money story you’d like to share? Get in touch by emailing money@gbnews.uk.

PrIme Minister Rishi Sunak has previously promised to bring inflation down to two per cent

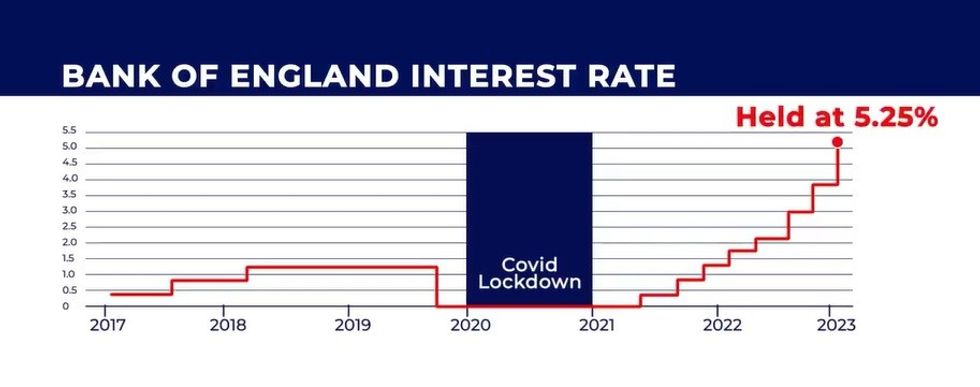

GETTYOver the last two years, the central bank has raised the country's base rate to 5.25 per cent in its fight to ease inflation with rates having been held at this level since August 2023.

Investec economist Sandra Horsfield said: “Welcome though a return to target inflation would be, the MPC (Monetary Policy Committee) is unlikely to be fully satisfied should the numbers meet our expectations.

“In the (Bank’s) May Monetary Policy Report, the baseline forecast was for a 1.9 per cent inflation rate.

“Nor it is clear that inflation will stay at two per cent from now on – In fact, we expect a small rise again over the second half of the year.”

Tobias Gruber, the founder and CEO of My Community Finance, added:: “Inflation is finally under control, but uncertainty remains about the Bank of England's base rate decision tomorrow.

"Savers should act now because while many savings rates are currently beating inflation, the best easy-access deals are vanishing fast. Rates are dropping as savings providers anticipate a rate cut later this year, and when one provider makes a move, others quickly follow suit.

"There are still excellent opportunities for fixed-rate savings, with some providers offering interest rates of over five per cent.

"If you don't need immediate access to your money, locking in a competitive fixed rate now can protect you from future base rate cuts. Just make sure you have emergency savings accessible because fixed-rate saving accounts typically don't allow withdrawals until your term ends.”

Savers have benefited from the Bank of England's decision to raise interest rates but this has had a detrimental impact on homeowners and other debt borrowers.

Millions of households have been forced to grapple with hiked mortgage and debt repayments as consequence of the MPC's decision-making

LATEST DEVELOPMENTS:

The Bank of England base rate has held interest rates at a 16-year high since it was hiked to 5.25 per cent last August GB NEWS

The Bank of England base rate has held interest rates at a 16-year high since it was hiked to 5.25 per cent last August GB NEWSReacting to today's CPI announcement, Shadow Chancellor Rachel Reeves said: "After 14 years of economic chaos under the Conservatives, working people are worse off. Prices have risen in the shops, mortgage bills are higher and taxes are at a 70-year high."

Liberal Democrat Treasury spokeswoman Sarah Olney said: “The hard truth is that millions of people won’t be feeling any better off today, thanks to years of Conservative economic mismanagement.

“Rishi Sunak’s boasts will ring hollow to countless families seeing their mortgages skyrocket and agonising rises in shopping prices compared to just a few years ago."

Work and Pensions Secretary Mel Stride told Times Radio: “We’re doing the right things for the economy and as you’ve just heard there, in terms of inflation now, very significant news this morning.

“That is now down at two per cent. That is bang on the Bank of England’s target of two per cent. You’ll recall back in the autumn, it was up above 11 per cent. And the Prime Minister quite rightly made it his key priority to get that figure down.”