A comfortable retirement costs £4,200 more a year than it did in 2022, according to new calculations.

Pensioners now need a total income of £47,700 in July 2023 for a comfortable retirement compared to £43,500 in April 2022, analysis from interactive investor suggests.

Assuming a retiree gets a full new state pension of £10,600, it would mean they need £37,100 private pension income, compared to £32,900 in April 2022.

To generate £4,200 additional pension income, pensioners would need a private pension pot of around £598,700 - £68,700 more than the £530,000 needed in April 2022.

High inflation over the last 18 months has had a 'devasting impact on the spending power of people’s pension income', Alice Guy said

|PEXELS

Alice Guy, head of pensions and savings at interactive investor said: “High inflation over the last 18 months has had a devasting impact on the spending power of people’s pension income, meaning that they need a lot more pension income just to maintain the same spending power.

“It now costs around £4,000 more for a comfortable retirement than in April 2022, due to persistently high inflation. And pensioners will need at least an extra £69,000 in their workplace or private pension pot to achieve that level of pension income.”

The calculations, based on the 2022 PLSA Retirement Living Standards (which were based on inflation up to April 2022), take account of inflation up to July 2023.

The private pension pot needed to generate enough pension income is based on the same assumptions used by the PLSA calculations, but interactive investor warned that in reality, most pensioners choose income drawdown rather than an annuity so the actual pension pot needed may be slightly different.

The analysts said for the “minimum” standard of living, the total pension income needed would now be £14,300 a year – a rise of £1,400.

The “moderate” level, which the PLSA said was £26,000 last year, would now be £28,600, interactive investor said.

Ms Guy said: “For a moderate retirement, pension savers will need a private pension income of around £2,600 more than last year and £42,800 more in their workplace or private pension pot.

"Those with a minimum pension income will need a scary 61 per cent more private pension income compared to last year just to keep up the same living standard and more than £23,000 more in their pension pot.

“These kinds of eye-watering sums are simply unaffordable for pensioners, many of whom have a small private pension pot and little option to make more pension contributions.

“The danger is that withdrawing more from your pension pot could have a long-term impact on your pension wealth – withdrawing too much could mean some pensioners run out of money earlier than planned.

"A minority of pensioners have an inflation-proof final salary pension, but even final salary pensions often have increases capped at three per cent or five per cent, so pensioners will have to make their money stretch further in times of high inflation.

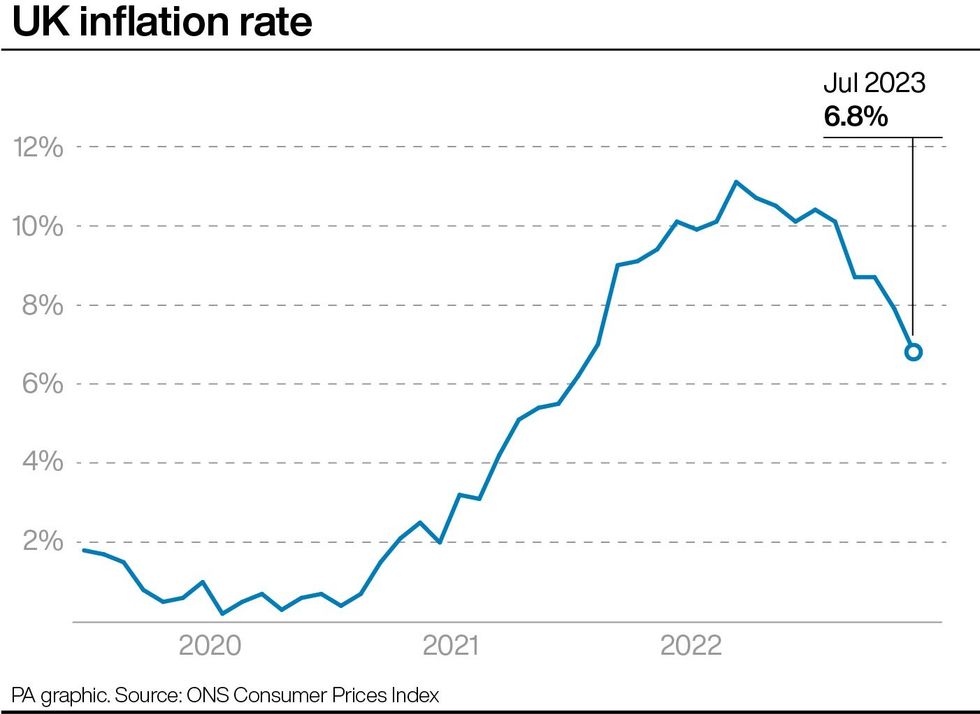

“While past performance is not an indicator of future results, pension savers can be encouraged that share prices have a rich history of outperforming inflation. There are also signs that high inflation is beginning to ease. The Bank of England expects inflation to fall to around three per cent by the middle of 2024.”

Nigel Peaple, director of policy and advocacy at the PLSA, told GB News: “The good news is that a combination of a full state pension and modest savings in a private or workplace pension will get most people to the level of the Minimum Retirement Living Standard, which will meet all of your basic needs.

LATEST DEVELOPMENTS:

UK CPI inflation has been easing in recent months

|PA

"For people retiring today, higher interest rates also mean you don’t need to have saved as much to secure the same level of income through an annuity as you would have even just a few months ago.

“However, at the minimum pension savings rates currently prescribed under the UK system, many people won’t save enough to achieve the retirement they might expect."

Mr Peaple urged a change in pension policy so employers help people to save more. The PLSA is calling on the Government to gradually increase automatic enrolment saving from eight per cent up to around 12 per cent, after the cost of living crisis has eased in the later 2020s.

Mr Peaple said: “We want to see a move to a 50/50 split, so employers pay in the same as their employees.

“If the UK does not increase its pension saving, many more people will fail to have the pension income they have hoped for and be left with no choice but to keep working late into their 60s.”

For pensioners who are struggling to make ends meet, checking eligibility for support such as Pension Credit is crucial.

Ms Guy said: “If you are struggling to make your pension income stretch it’s important to check if you could be entitled to benefits like pension credit. It’s estimated that around 800,000 pensioners currently aren’t claiming Pension Credit who could be entitled and the average claim is worth around £3,500.

“It’s also important to make the most of any private pension income. Check your pension fees and investment performance as some pension schemes charge much more than others.

“It may also be worth consolidating small pension pots to make your pension easier to manage, although it’s important to take advice to make sure you won’t lose out on any important benefits by transferring.”