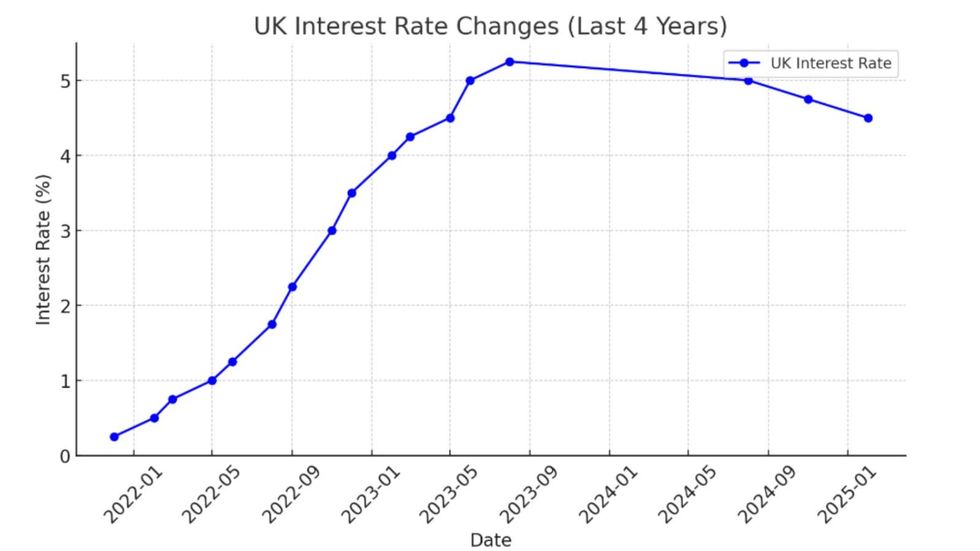

The Bank of England has decided to keep interest rates at 4.5 per cent, dashing hopes of relief for homeowners facing soaring mortgage costs.

Millions of borrowers are still paying interest rates as high as eight per cent , with no clear sign of when the bank rate will ease.

Alastair Douglas, TotallyMoney CEO said: "If you’re waiting for a rate cut to remortgage, then you might be better off locking in a new deal before your bank puts you onto their Standard Variable Rate.

"The is currently 6.75 per cent but you could find yourself paying upwards of eight per cent. Banks are already likely to have already factored future rate cuts into their pricing, so we might not see any big changes if and when the MPC makes its next move."

At its meeting today the MPC voted by a majority of 8–1 to maintain Bank Rate at 4.5 per cent. One member preferred to reduce Bank Rate by 0.25 percentage points, to 4.25 per cent.

The Bank rate plays a crucial role in shaping borrowing costs for households, businesses, and the government, while also impacting returns for savers.

While no change was expected at today's meeting, many analysts are forecasting two further cuts by the end of the year.

The Bank of England's decision over interest rates will impact mortgages GETTY

The Bank of England's decision over interest rates will impact mortgages GETTY The Bank of England is responsible for bringing inflation down to two per cent, but the latest data shows it rose to three per cent in January, strengthening expectations that interest rates would stay unchanged.

Cutting rates now could encourage consumer spending, potentially driving inflation even higher. That could be a blow to some homeowners who would like to see interest rates and, in turn, mortgage rates continue to fall.

Before the annoucnement, Paul Heywood, chief data and analytics officer at credit agency Equifax UK said: "Bank of England policymakers have been warning on inflation and lingering uncertainty, so further rate-cutting relief for homeowners looks to be an unlikely outcome from this month's meeting."

According to UK Finance, approximately 1.1 million households are currently on their lender’s standard variable rate (SVR).

If interest rates are increased, lenders can choose to increase its SVR, borrowers on these rates may see their repayments rise. However, lenders are not obligated to pass on rate cuts in full—or at all.

Interest rates have skyrocketed in recent years due to the Bank of England's decison-making CHATGPT

Interest rates have skyrocketed in recent years due to the Bank of England's decison-making CHATGPTThe average standard variable rate (SVR) has fallen further below eight per cent month-on-month and stands at 7.68 per cent, down from 8.18 per cent a year ago.

Rachel Springall, Finance Expert at Moneyfactscompare.co.uk, said: "Despite consecutive falls to the average Standard Variable Rate (SVR), the incentive to switch remains as a typical mortgage borrower being charged the current average SVR of 7.68 per cent would be paying £358 more per month, compared to a typical two-year fixed rate."

SVRs can be significantly more expensive than fixed or tracker mortgage deals. Borrowers on these rates are advised to review their mortgage options to determine whether remortgaging could offer potential savings.

If the Bank cut rates now, it could encourage consumer spending, potentially driving inflation even higher

GETTYSince March 2024, the average two-year fixed rate has fallen from 5.76 per cent to 5.39 per cent and the average five-year fixed rate has fallen from 5.34 per cent to 5.22 per cent; both are down month-on-month.

These average rates were 5.52 per cent and 5.32 per cent respectively last month. On a 10-year fixed rate mortgage, the average rate was 5.98 per cent in March 2024. This rate has fallen to 5.61 per cent and is down month-on-month.

Alice Haine, Personal Finance Analyst at Bestinvest by Evelyn Partners said: “Keeping the headline interest rate on hold will be a blow for mortgaged homeowners and first-time buyers hoping for further respite from high borrowing costs.

"While three rate reductions since last August have provided some relief from the sky-high borrowing costs of the past few years, it won’t have solved all the affordability challenges existing homeowners and prospective buyers are still facing."

Next week, Chancellor Rachel Reeves will present her Spring Statement, which is not expected to include major policy changes but will provide an update from the Office for Budget Responsibility on the state of the UK economy.