Millions of savers could lose up to £35,000 in retirement savings after Chancellor Rachel Reeves put the second phase of a crucial pensions review on hold indefinitely.

The delay comes amid concerns about adding financial pressure on businesses, following backlash over the Budget's £25bn national insurance contributions bill for employers.

Emma Reynolds, pensions minister had promised to launch a review examining retirement savings adequacy before the end of the year, but this has now been suspended with no new timeline.

Pension experts warn the postponement could severely compromise "better retirement prospects for millions" of Britons, with current contribution rates already deemed insufficient for adequate retirement income.

"A prolonged, open-ended delay will be damaging for industry confidence," warns Calum Cooper, Head of Pensions Policy Innovation at Hymans Robertson.

Sir Steve Webb, former pensions minister and a consultant at LCP, said the delay was “deeply depressing” as it could result in “yet more wasted years”.

Under current auto-enrolment rules, staff must contribute at least eight per cent of qualifying earnings into workplace pensions annually, with employers required to provide at least three per cent. But many experts believe these rates are insufficient to secure adequate retirement incomes.

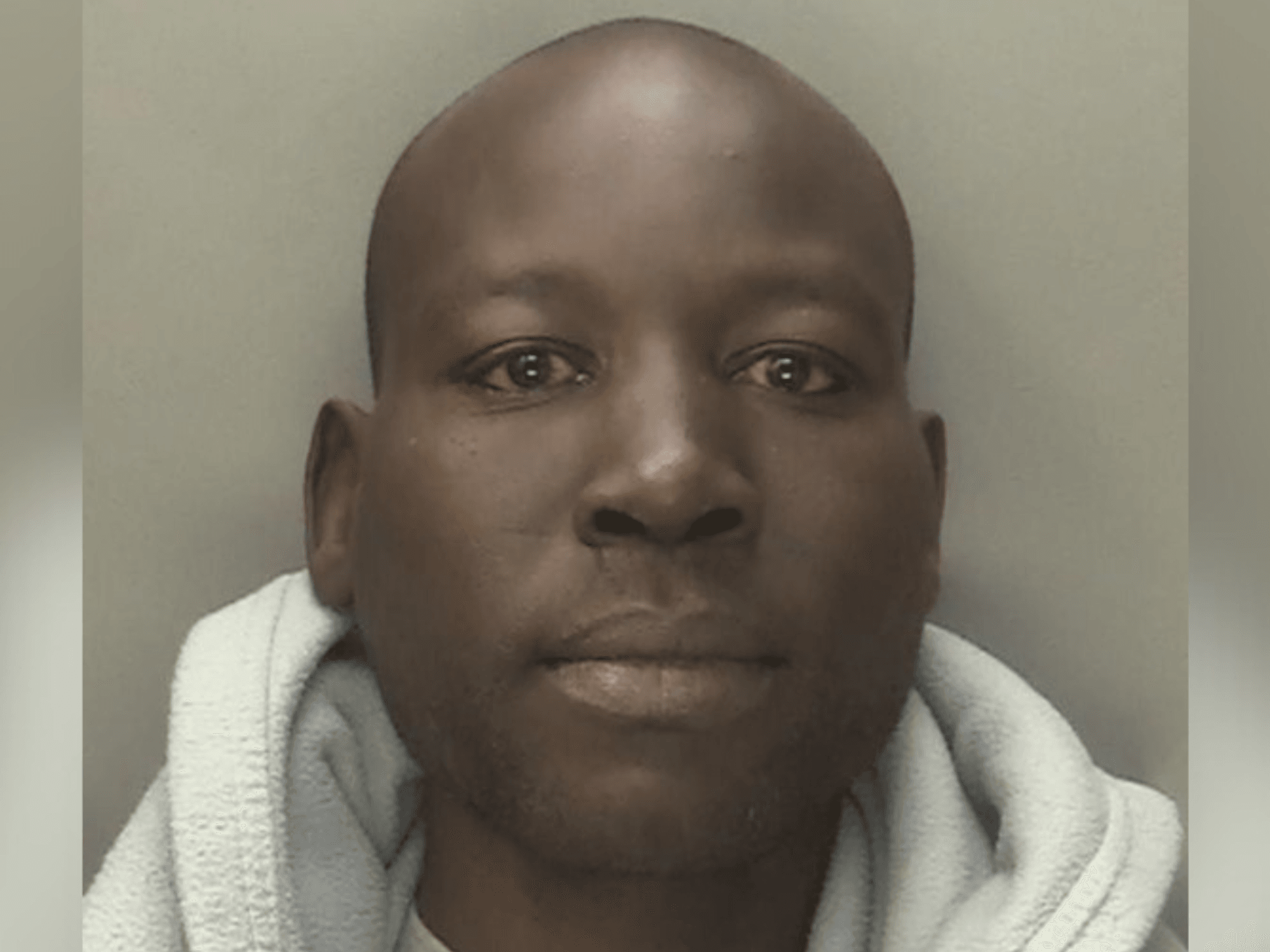

Pensioners are finding themselves with not enough saved for retirement | GETTY

Pensioners are finding themselves with not enough saved for retirement | GETTY Phoenix Group analysis found that for a typical 18-year-old, increasing minimum auto-enrolment contributions from eight per cent to 12 per cent could lead to almost £96,000 extra in their pension pot (in today’s money terms) at state pension age, equivalent to £64/week.

However, delaying this increase by five years, reduces the total additional savings potential by nearly £10,000. A 10-year delay reduces the additional savings potential by around £22,000, and a 15-year delay by £35,000.

Catherine Foot, Director of Phoenix Insights said: "Hitting pause on the retirement adequacy review could be hugely detrimental to people’s financial future. In the next five years, the majority of defined contribution pension savers will enter retirement with less income than they expect or need, and this will worsen to a peak in the early 2040s.

“There are clearly some valid concerns around what increases to auto-enrolment contributions might mean for businesses, but that shouldn’t stop analysis and consensus-building on how and when we address the retirement crisis unfolding before our eyes. Increasing minimum auto-enrolment contributions is one of the biggest levers to tackle undersaving and we cannot afford to delay setting out a plan to incrementally raise contributions.

“The adequacy review is a golden opportunity to look at the retirement landscape as a whole and prevent serious problems for individuals and the state in years to come. With the impending retirement crisis about to unfold, the review should not be kicked into the long grass.”

LATEST DEVELOPMENTS:

Research from the Institute for Fiscal Studies reveals that 30 to 40 per cent of savers in defined contribution schemes are heading towards retirement incomes below the minimum living standard.

The Pensions and Lifetime Savings Association (PLSA) has urged the Government to gradually increase minimum auto-enrolment contributions to around 12 per cent of salary.

Speaking on the delay of the pension review, Cooper strongly criticised the Government's decision, stating that the delay "ends weeks of hope" for meaningful pension reform.

He said: "Retirement adequacy is an enormous issue for savers heading towards retirement, and in turn this will remain an ongoing concern for future governments and UK society as a whole. There should be nothing to fear from undertaking a meaningful pension review to tackle the adequacy challenge."

Cooper warns that the lack of timescale could add months and years to implementing crucial decisions, with impacts measured in generations.

While acknowledging short-term benefits for businesses, Cooper argues the Government could start the review immediately with any impact delayed until a future date.

He urges the Government to use this delay productively by establishing an independent pensions commission to work across the political spectrum.

He said: "This will give the best chance of leaving behind better jobs and a UK pensions system to be proud of from the Labour Government."

Helen Morrissey, head of retirement analysis at Hargreaves Lansdown, describes the review delay as "disappointing," emphasising the urgency of addressing pension adequacy.

She explained that the issue of adequacy is vital and it's a discussion that needs to happen sooner rather than later, whilst acknowledging current pressures on employers and households. She stresses the review should establish a long-term savings framework.

Recent findings from Hargreaves Lansdown's Savings and Resilience Barometer reveal only 38 per cent of households are on track for a moderate retirement income.

She said: "Ultimately people need confidence in the pension system and to know that they are putting enough away to see them through retirement. We can't keep kicking the can down the road."

The Department for Work and Pensions (DWP) insists the second phase has not been "long-grassed" but offers no new launch date.

A DWP spokesperson said: "Government will set out more details on the second phase in due course,"